Encouraging Export Diversification for Canadian Small and Medium-Sized Businesses: Quantitative and Qualitative Research on Free Trade Agreements

Final Report

Prepared for Global Affairs Canada

Supplier Name: Phoenix SPI

Contract Number: 08915-180520/001/CY

Contract Value: $132,465.95 (including HST)

Award Date: 2019-01-31

Delivery Date: 2019-06-03

Registration Number: POR 115-18

For more information on this report, please contact Global Affairs Canada at: POR-ROP@international.gc.ca

Ce rapport est aussi disponible en français.

Encouraging Export Diversification for Canadian Small and Medium-Sized Businesses: Quantitative and Qualitative Research on Free Trade Agreements

Final Report

Prepared for Global Affairs Canada

Supplier name: Phoenix Strategic Perspectives Inc.

June 2019

This public opinion research report presents the results of an online survey of 507 export-oriented companies and set of 40 in-depth telephone interviews conducted by Phoenix SPI on behalf of Global Affairs Canada. The fieldwork for the research took place between March and April 2019.

This publication may be reproduced for non-commercial purposes only. Prior written permission must be obtained from Global Affairs Canada. For more information on this report, please contact Global Affairs Canada at:

Communications Branch

Public Services and Procurement Canada

Portage III Tower A

16A1-11 Laurier Street

Gatineau QC K1A 0S5

Catalogue number:

FR5-159/2019E-PDF

International Standard Book Number (ISBN):

978-0-660-30924-8

Related publications (registration number: POR 115-18):

Catalogue number FR5-159/2019F-PDF (Final report, French)

ISBN 978-0-660-30925-5

© Her Majesty the Queen in Right of Canada, as represented by the Minister of Foreign Affairs, Canada, 2019

Cette publication est aussi disponible en français sous le titre : Promouvoir la diversification des exportations des petites et moyennes entreprises canadiennes: une recherche quantitative et qualitative sur les accords de libre-échange.

Table of Contents

List of Figures

Executive Summary

Phoenix Strategic Perspectives Inc. (Phoenix SPI) was commissioned by Global Affairs Canada (GAC) to conduct quantitative and qualitative research in support of export diversification.

Background and Objectives

In alignment with the Minister of International Trade Diversification’s mandate letter, GAC is pursuing efforts to help Canadian companies diversify their exports abroad. The Free Trade Agreement Promotion Task Force was established to promote Free Trade Agreements (FTAs) through outreach to Canadian companies and training Canada’s trade commissioners. The Task Force had been in place for three years. GAC, therefore, wanted to collect baseline data on Canadian small and medium-sized businesses’ (SMEs) awareness of Canada’s FTAs, the extent to which these businesses are taking advantage of FTAs already in place, and the challenges SMEs see vis-à-vis diversifying their export markets.

The objectives of the research were to determine:

- Canadian SMEs’ awareness of Canada’s free trade agreements, with a focus on the Canada-EU Comprehensive Economic and Trade Agreement (CETA), the Comprehensive and Progressive Trans-Pacific Partnership (CPTPP), the Canada-Korea Free Trade Agreement, the Canada-Israel Free Trade Agreement, and the Canada-Ukraine Free Trade Agreement;

- businesses’ intentions regarding FTA utilization;

- the level of understanding by SMEs of the benefits and requirements of Canada’s FTAs (in terms of tariffs, rules of origin, procurement, labour mobility etc.);

- Canadian SMEs’ experience using FTAs, including the impact of FTAs on decision processes, and the barriers that prevent businesses from using FTAs;

- what information and programming support Canadian companies require to diversify their exports; and

- from which sources Canadian companies prefer to receive business-related information.

The findings from this research will be used by GAC to shape its FTA promotion strategy to better meet the needs of SMEs and provide a better client experience for Canadian companies that would like to diversify their exports.

Methodology

Qualitative and quantitative research was conducted with the target population: Canadian SMEs that export. This included an online survey administered to 507 Canadian SMEs that export and a set of 40 in-depth, one-on-one telephone interviews conducted with a sub-sample of survey respondents. Specifically:

- The online survey averaged 15 minutes to complete. The sample was drawn from the business panels of Dynata and Maru/Blue. Panellists were invited to participate in the survey through an email invitation which contained a password-protected URL to access the survey. Survey data was weighted by region and business size to reflect the composition of the target population. Surveys that use samples drawn from online panels cannot be described as statistically projectable to the target population. No estimates of sampling error can be calculated because the sample is based on those who initially self-selected for participation in the panel. The fieldwork was conducted between March 19 and April 1, 2019.

- A set of 40 in-depth, one-on-one telephone interviews were conducted with a sub-sample of survey respondents. Interviews were conducted in the individuals’ official language and averaged approximately 30 minutes. All interviews were completed between March 28 and April 10, 2019. Participants received an honorarium of $150 in appreciation of their time.

Additional methodological information is available in the appendix.

Summary of Findings

Exporting Activities

Majority of SMEs export to the U.S. and other foreign markets.

-

More than half (59%) the companies surveyed export to the United States (U.S.) and other foreign markets. In contrast, approximately three in ten (29%) export only to the U.S. and 12% to foreign markets, excluding the United States.

- Most interview participants indicated that their company began with a domestic focus and then later developed an international focus. Reasons for companies to begin immediately with an international focus included: the fact that the markets for the company’s products are primarily outside Canada, the opportunity to ‘piggy-back’ on large international companies, the need for larger market opportunities to offset production costs, and personal experience or contacts.

- Among companies that export goods or services, North America (71%) is the top destination, followed by Europe (67%) and the Asia-Pacific region (55%). Fewer companies currently export to countries in Central or South America (27%) and to the Middle East or Africa (22%).

-

At the country level:

- The U.S. (97%) is the top export destination among companies that currently export to North America.

- The United Kingdom (55%), followed by France (41%), and Germany (38%) are the top destinations among companies that currently export to Europe.

- Among companies currently exporting to Asia-Pacific region, 49% export to Australia. Following Australia are China (36%), Japan (32%), New Zealand (26%), Hong Kong (20%), India (20%) and Taiwan (17%).

- Brazil is the top export destination in Central and South America—42% of respondents said their company currently exports to Brazil, while 26% export to Chile, 22% to Argentina, and 22% to Colombia.

- The United Arab Emirates (36%), Israel (35%), and South Africa (32%) are top export destinations in the Middle East and Africa.

- In terms of export diversification, one-third of companies are not interested in any other markets at this time. Among those companies that are planning to enter new markets, Australia (20%), followed by New Zealand (15%) and the United Kingdom (14%), were the top destinations.

Exporting Obstacles and Assistance

Canadian SMEs face numerous challenges in relation to their activities in international markets.

-

The value of the Canadian dollar is the top challenge experienced by companies—for 69% of companies, it is at least a minor obstacle to their company’s activities in international markets. Other challenges experienced by majorities of companies when it comes to their activities in international markets include: uncertainty of the regulatory requirements in other countries (67%), lack of market contacts (64%), foreign tariffs and trade barriers (63%), lack of information on business opportunities (62%), linguistic or cultural obstacles (57%), lack of access to financing and funding (53%), and Canadian export taxes or permits (53%).

- Interview participants echoed, as well as elaborated on, these challenges. In particular, for smaller firms, and companies that recently started international activities, making connections and networking as well as financial assistance were described as important challenges—the former because it is important to have knowledgeable ‘people on the ground’ to facilitate entry into a foreign market, and the latter because smaller firms many not have the cash flow available to support international business opportunities.

Canadian SMEs require at least a little assistance in many areas when developing business in markets outside of Canada.

-

Areas in which Canadian SMEs were more likely to require some or a great deal of assistance include market intelligence and information (48%), referrals to international sales leads (47%), understanding business practices in foreign markets (45%), and information about companies in foreign markets (43%).

- Interview participants provided more detailed insights into the types of assistance that would help their company address challenges related to their international business activities.Specifically, participants mentioned advice on legal issues, taxation, use of free trade agreements, international standards for products and services, and general information about how to operate in different regions.

- Other types of assistance mentioned with frequency were financial assistance to help expand to international markets, foreign contacts to implement market plans (“boots on ground”), competitive intelligence, as well as business leads and foreign contacts.

- Areas in which companies are less likely to require assistance are referrals of technology and/or R&D partnership opportunities (47% of companies require no assistance), information or advice on locating financial/funding assistance financial advice (45% require no assistance), and practical advice on timing and organizing your business trip (44% require no assistance).

Awareness and Use of Free Trade Agreements

Among Canadian SMEs, there was fairly low awareness of Canada’s free trade agreements.

- Representatives of exporting companies were most likely to be aware of the Comprehensive and Progressive Trans-Pacific Partnership (CPTPP) (74%) and the Canada-European Union Comprehensive Economic and Trade Agreement (CETA) (72%). That said, only 7% of respondents said they are aware of the details of these free trade agreements.

- The majority of respondents have never heard about the Canada-Ukraine Free Trade Agreement (CUFTA) (64%), Canada-Israel Free Trade Agreement (CIFTA) (57%), Modernized Canada-Chile Free Trade Agreement (CCFTA) (54%), and Canada-Korea Free Trade Agreement (CKFTA) (52%).

Few companies use any of these free trade agreements; the exception is NAFTA.

- One-third (33%) of companies currently use the North American Free Trade Agreement (NAFTA) and 22% said their company is planning to start using the agreement in the next year.

- Nine percent of surveyed companies use CETA and 17% are planning to use this agreement, while 7% use CKFTA and 14% are planning to use it. Seven percent of companies are using the Canada-European Free Trade Association Free Trade Agreement and 20% are planning to use the agreement in the next year. Five percent are using CUFTA, CCFTA, and CIFTA.

- The majority of companies are not using and have no plans to use the following free trade agreements: Canada-Honduras Free Trade Agreement (65%), Canada-Jordan Free Trade Agreement (65%), Canada-Colombia Free Trade Agreement (63%), Canada-Peru Free Trade Agreement (60%), Canada-Costa Rica Free Trade Agreement (60%), and Canada-Panama Free Trade Agreement (56%).

-

Topping the list of reasons why companies do not use Canada’s free trade agreements were perceptions that there is no benefit for their company to be derived from using a free trade agreement (34%) and that free trade agreements are difficult to take advantage (30%).

- Among interview participants, the following reasons were offered: free trade agreements do not apply to them (the assumption being that such agreements apply exclusively or mainly to providers of goods or products); their line of business is unaffected by free trade agreements (e.g., photography, publishing, consulting); lack of need; company size (i.e., the perception that free trade agreements are designed for large companies); and lack of information.

Impact of Free Trade Agreements

Tariff reduction is the top perceived benefit of using free trade agreements.

-

Nearly six in 10 (58%) companies that use free trade agreements have benefited from tariff reduction or elimination on goods. Significantly fewer have benefitted from better conditions for exporting services (23%), easier access to government procurement opportunities (20%), greater business stability due to investment clauses in the agreement (17%), and labour mobility clauses/temporary entry (16%).

- When interview participants were asked about the benefits of free trade agreements, there was a noteworthy difference in feedback by the type of exporter. While companies exporting goods could readily identify benefits (e.g., business expansion, client diversification, access to new markets, increased profits, etc.), most service providers said that free trade agreements apply primarily or exclusively to products not services.

- Challenges of free trade agreements were also identified by interview participants: increased competition domestically and internationally, unfair trade practices (e.g., protectionism, corruption), and understanding the terms of the agreements (e.g., which products and services are included, how to settle disputes), among others.

Free trade agreements influence companies’ export strategy in various ways.

- Most respondents said free trade agreements influence their company’s export strategy at least a small amount. Specifically, 14% are influenced a great deal by free trade agreements, 27% a moderate amount, and 33% a small amount.

Communication Preferences and Information Needs

Top information sources for doing business abroad – associations and colleagues.

-

When asked where they get their information and advice on doing business abroad, such as exporting and using free trade agreements, approximately one-third each mentioned industry or business associations (32%) and business associates, colleagues, or partners (32%). Twenty-nine percent use the websites or free online tools of trade promotion organizations.

- Interview participants pointed to the following information needs: market analyses, strategic advice on entering foreign markets, ‘dos and don’ts’ of conducting business in a country or region, information on the political climate in a country or region, advice on risk management, business leads and foreign contacts, and information about international rules, regulations, policies, among others.

- Their main challenges in obtaining this type of information are lack of time, lack of expertise, lack of qualified staff (or resources in general), costs, and getting information in a timely manner,

Vast majority uses the internet to stay on top of industry trends and general business information.

- Just over three-quarters (77%) of respondents said they look to the internet when it comes to staying on top of industry trends and general business information. Following this, 46% use social media.

Reading articles, getting answers from experts – top methods to consume information

- When learning or researching something new, 59% of respondents prefer to read articles and 46% to get answers from an expert.

Notes to Readers

- The report is divided into two sections. The first section presents the results of the online survey (the quantitative component), and the second section presents the results of the in-depth interviews (the qualitative component).

-

Regarding the qualitative results:

- The results provide an indication of participants’ views about the issues explored, but they cannot be generalized to the full population of Canadian SMEs that export.

-

Regarding the quantitative results:

- All results in the report are expressed as percentages, unless otherwise noted. Throughout the report, percentages may not always add to 100% due to rounding.

- In graphs, “DK” stands for “Don’t know” and “NR” for “No response.”

-

Where base sizes are reported in tables and graphs, they reflect the actual number of respondents who answered or were asked the question.

- The number of respondents changes throughout the report because questions were asked of sub-samples of survey respondents. Readers should be aware of this and exercise caution when interpreting results based on smaller numbers of respondents.

-

Subgroup differences are identified in the report. When reporting subgroup variations, only differences that are significant at the 95% confidence level are discussed in the report. If one or more categories in a subgroup are not mentioned in a discussion of subgroup differences, it can be assumed that significant differences were found only among the categories reported.

- When reporting differences by business size, a micro-firm is a firm that has fewer than 5 employees, a small firm has 5-99 employees, a medium firm has 100-499 employees, and a large firm has 500+ employees.

- The results are reflective of Canadian SMEs that export, but they cannot be considered representative of the target population because random sampling was not used. When non-probability sampling is used, the extent to which the survey sample represents the target population is not known (because probability theory cannot be applied).

- The tabulated data is available under separate cover and the research instruments can be found in the appendix.

The contract value was $132,465.95 (including HST).

Political Neutrality Certification

I hereby certify as a Senior Officer of Phoenix Strategic Perspectives that the deliverables fully comply with the Government of Canada political neutrality requirements outlined in the Communications Policy of the Government of Canada and Procedures for Planning and Contracting Public Opinion Research. Specifically, the deliverables do not contain any reference to electoral voting intentions, political party preferences, standings with the electorate, or ratings of the performance of a political party or its leader.

Signed:

Alethea Woods, President

Phoenix Strategic Perspectives Inc.

Detailed Findings

Phase 1: Online Survey

I. Corporate Profile

This section presents the characteristics of survey participants and their businesses.

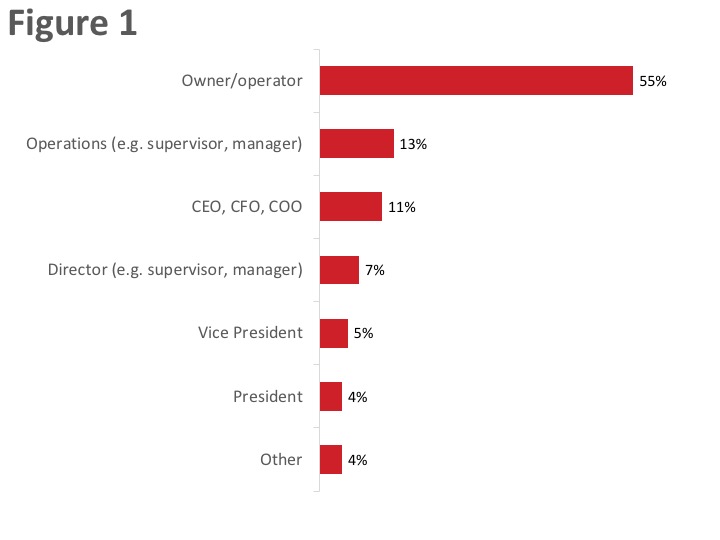

Majority of respondents are owners

Fifty-five percent of respondents are owners. The rest are managers or supervisors in operations (13%), c-level executives (11%), directors (7%), vice presidents (5%), or presidents (4%) of their company.

Figure 1: Role of respondents

Text Description - Figure 1

Base: n=507; all respondents / S3. Which title best describes your role within the company?

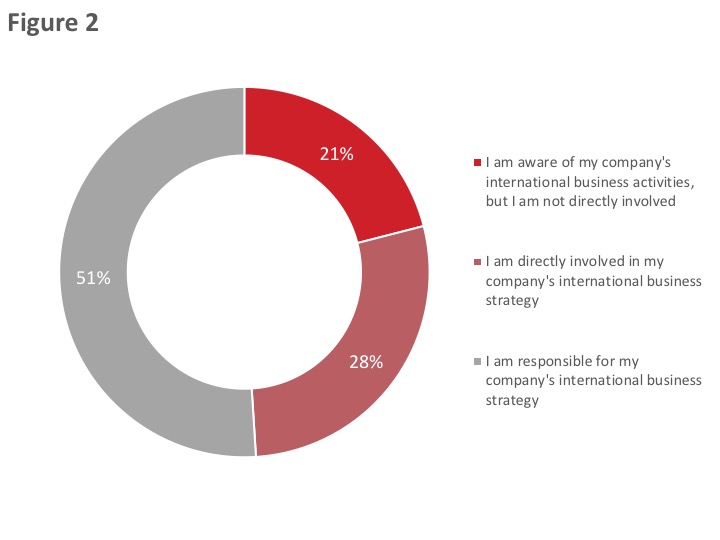

Most are responsible for or directly involved in their company’s international business activities

Half (51%) of those surveyed said they are responsible for their company’s international business strategy. Twenty-eight percent are not responsible, but they are directly involved in their company’s strategy. One in five (21%) are aware of their company’s activities but are not directly involved in such activities.

Figure 2: Familiarity with Company’s International Business Activities

Text Description - Figure 2

Base: n=507; all respondents / S4. How familiar are you with your company’s international business activities?

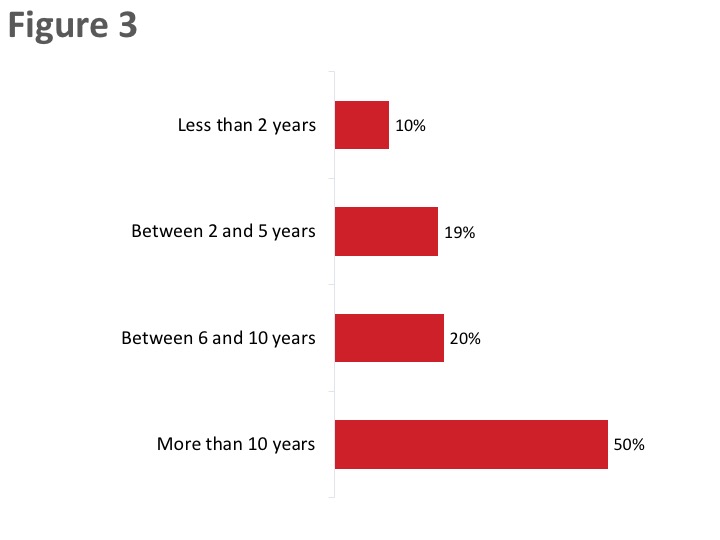

Most work for firms that are established exporters

Half (50%) the respondents said their company has been exporting goods or services internationally for more than 10 years. An additional 20% work for firms that have been exporting for six to 10 years. In total, therefore, 70% of those surveyed work for firms that have been exporting for at least six years. Approximately one in five (19%) said their firm has been exporting for two to five years, while 10% have been exporting for less than two years.

Figure 3: Length of Time Exporting

Text Description - Figure 3

Base: n=507; all respondents. [Dk/nr: 4%; n=17 removed] / A3. For how many years has your company been exporting goods or services internationally?

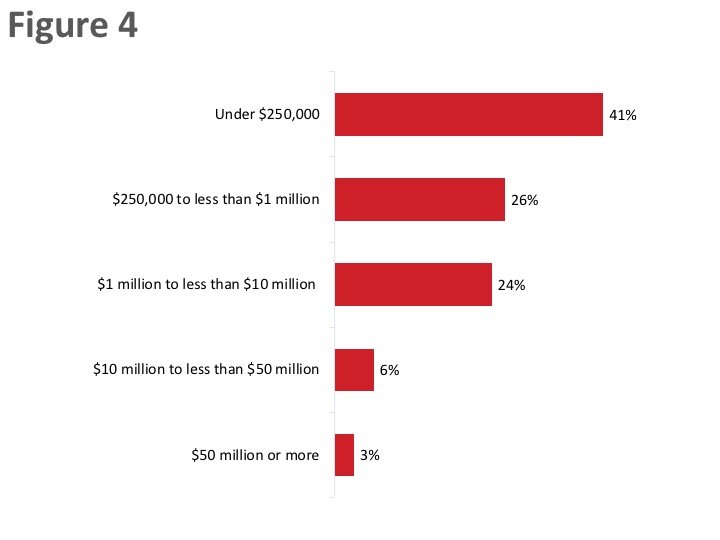

Company Revenues

Respondents were asked to identify their company’s total revenues in their last fiscal year. Two-thirds reported revenues under $1 million: 41% said their firm earned under $250,000 and 26% earned $250,000 to just under $1 million. Conversely, one-quarter (24%) had revenues between $1 million and just under $10 million, while 9% earned $10 million or more in their last fiscal year.

Figure 4: Company Revenues

Text Description - Figure 4

Base: n=507; all respondents. [Dk/nr: 13%; n=57 removed] / A2.In your last fiscal year, what were your company’s total revenues?

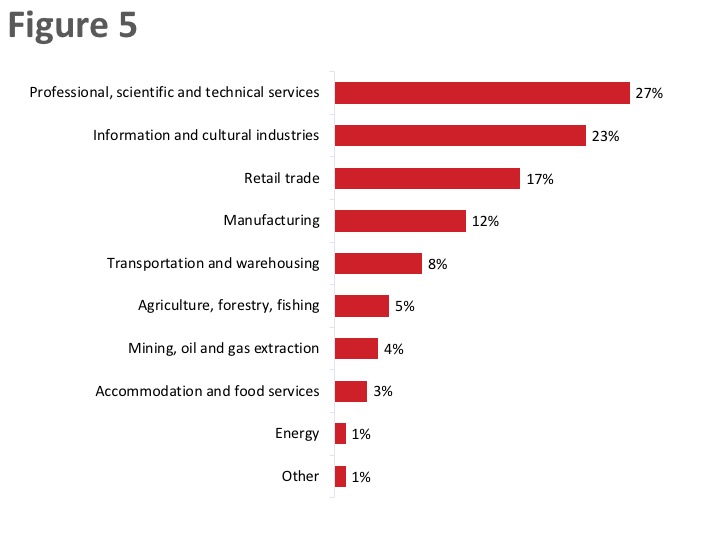

Industry/Sector

When asked to identify the main sector in which their company operates, the greatest single proportion of respondents (27%) said their firm operates in professional, scientific and technical services, followed by information and cultural industries (23%) and retail trade (17%). [1]

Figure 5: Industry/sector

Text Description - Figure 5

Base: n=507; all respondents. / A1. In which industry or sector does your company operate?

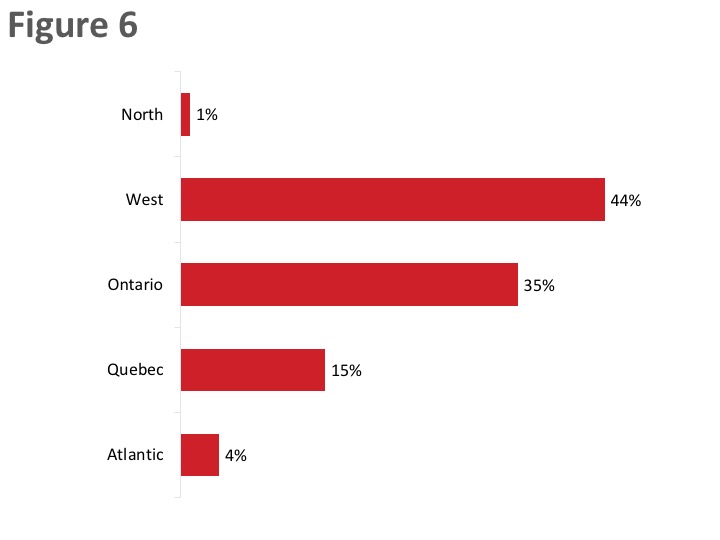

Company Headquarters

The largest proportion of companies are located in the West (44%), followed by Ontario (35%).

Figure 6: Headquarter Location

Text Description - Figure 6

Base: n=507; all respondents / S6. In which province or territory is your company’s headquarters located?

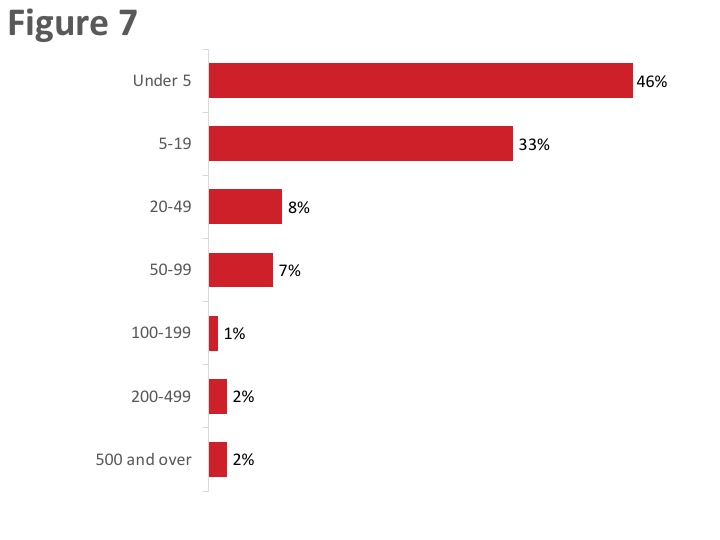

Number of Employees

Per the research design, virtually all respondents represented small or medium-sized Canadian companies.[2]

Figure 7: Number of employees

Text Description - Figure 7

Base: n=507; all respondents / S2. How many employees work for your company?

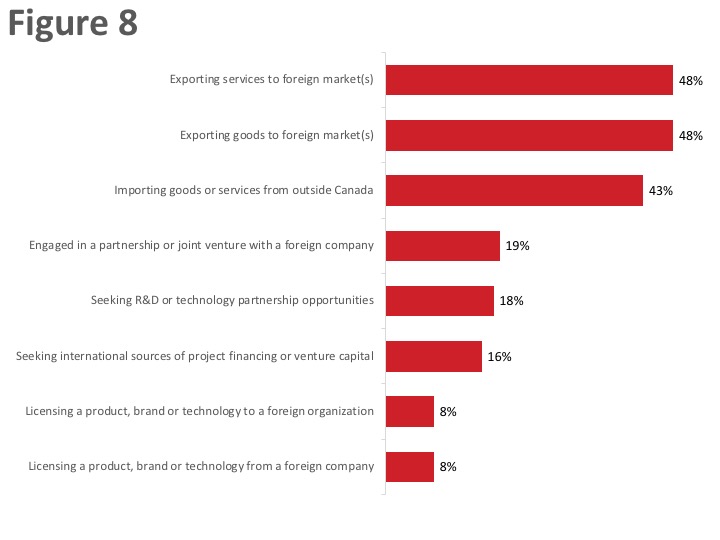

Companies more likely to export and import than be engaged in/looking for partnership or licensing opportunities

Survey respondents work in firms that are involved in international trade and investment in a variety of ways.

Figure 8: Company Trade Activities

Text Description - Figure 8

Base: n=507; all respondents. / S1. Is your company currently engaged in any of the following activities? (multiple responses accepted).

II. Exporting Profile

This section presents information about the exporting activities of surveyed companies.

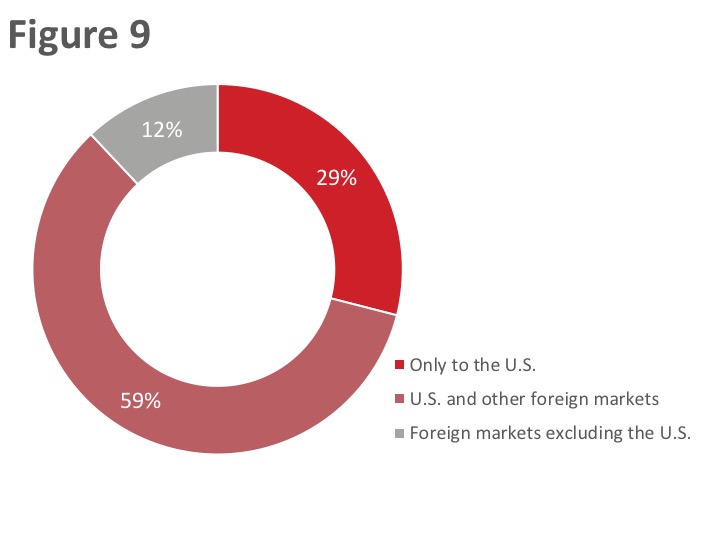

Majority exports to the U.S. and other foreign markets

More than half (59%) the companies surveyed export to the United States (U.S.) and other foreign markets. In contrast, approximately three in ten (29%) export only to the U.S. and 12% to foreign markets excluding the United States.

Figure 9: Export Markets

Text Description - Figure 9

Base: n=507; all respondents. [Dk/nr: 4%; n=19 removed] / B1. Does your organization export goods and services…?

The likelihood of exporting only to the U.S. was higher among small companies (35%) compared to micro-firms (24%).

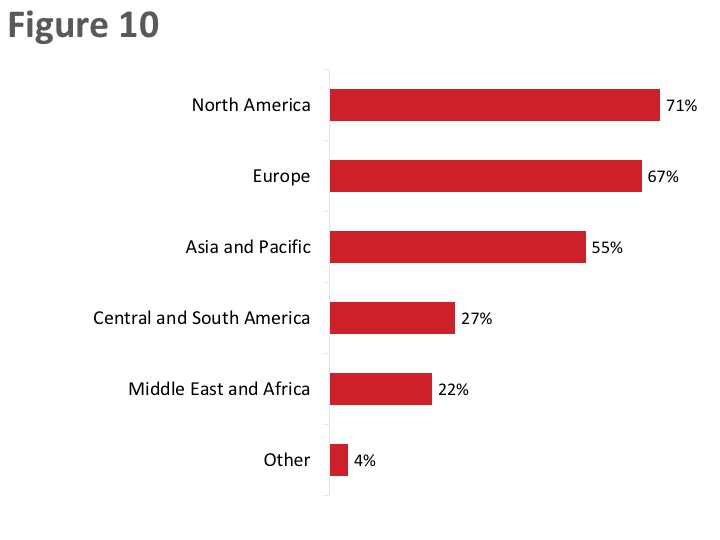

North America, followed by Europe and Asia/Pacific are the top export destinations

Among companies that export goods or services (n=348), North America (71%) is the top destination, followed by Europe (67%) and the Asia-Pacific region (55%). Fewer companies currently export to countries in Central or South America (27%) and to the Middle East or Africa (22%).

Figure 10: Current Export Markets

Text Description - Figure 10

Base: n=348; respondents who export goods and services to the US and foreign markets. [Dk/nr: 4%; n=15 removed] / B2. Which markets does your company currently export to? (multiple responses accepted).

The likelihood of exporting to North America was higher among small companies (77%) compared to micro-firms (65%), companies exporting goods (79%) compared to those exporting services (63%), companies that have been exporting for more than 10 years (75%) compared to companies that have been exporting for five or fewer years (61%), and companies active in the information and cultural industries sector (87%) compared those active in retail trades (62%) and professional, scientific and technical services (61%).

Companies exporting goods and services (83%) were more likely than companies exporting only services ( 60%) to export to countries in Europe. The same applied to companies aware of the Trade Commissioner Service (TCS): 82% of those aware of the TCS currently export to Europe compared to 60% of companies not aware of TCS.

The likelihood of exporting to countries in Asia and the Pacific was higher among companies that export goods only (67%) and goods and services (79%) compared to those that export only services (42%).

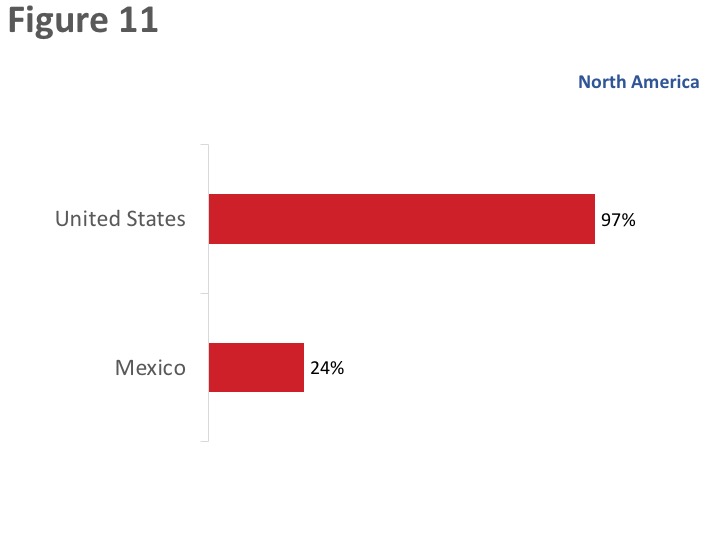

Top North American destination is the U.S.

The United States is the top export destination among companies that currently export to North America. Virtually everyone (97%) said their company exports to the U.S., while only one-quarter (24%) mentioned Mexico.

Figure 11: Current Export Markets: North America

Text Description - Figure 11

Base: n=240; respondents who export to North America. / B2. Which markets does your company currently export to? (multiple responses accepted).

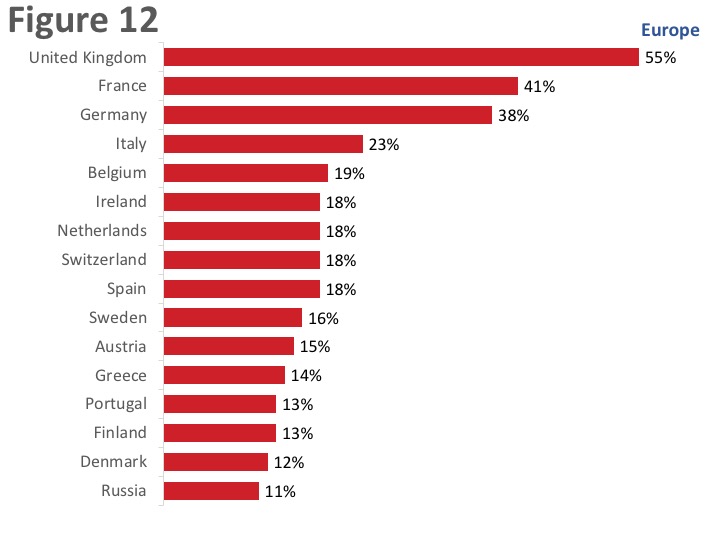

United Kingdom, France and Germany are the top European export destinations

The United Kingdom (55%), followed by France (41%), and Germany (38%) are the top destinations among companies that currently export to Europe. As the graph depicts, smaller proportions of companies currently export to a variety of other European countries.

Figure 12: Current Export Markets: Top European Destinations

Text Description - Figure 12

Base: n=234; respondents who export to Europe. / B2. Which markets does your company currently export to? (multiple responses accepted).

In addition, countries mentioned by fewer than one in 10 respondents include:

- Hungary (9%) and Poland (9%);

- Norway (8%);

- Luxembourg (7%), Czech Republic (7%), and Turkey (7%);

- Iceland (6%);

- Kazakhstan (5%), Romania (5%), and Ukraine (5%);

- Estonia (4%), Latvia (4%), Bulgaria (4%), Croatia (4%), Slovak Republic (4%) and Lithuania (4%); and

- Malta (3%), Cyprus (3%), Serbia (3%), and Slovenia (3%).

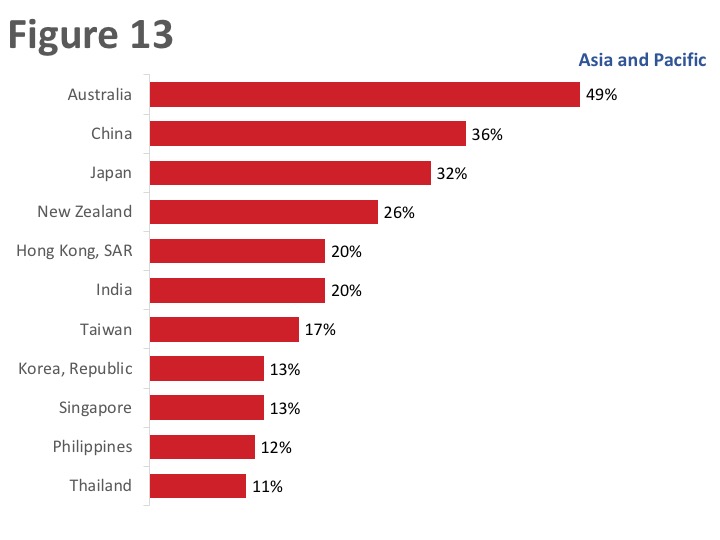

Australia is the top export destinations in Asia and the Pacific

Almost half (49%) the companies surveyed currently export to Australia. Following Australia are China (36%), Japan (32%), New Zealand (26%), Hong Kong (20%), India (20%) and Taiwan (17%). As the graph depicts, smaller proportions of companies export to a variety of other countries in Asia and the Pacific.

Figure 13: Current Export Markets: Top Asia and Pacific Destinations

Text Description - Figure 13

Base: n=195; respondents who export to Asia and the Pacific. / B2. Which markets does your company currently export to? (multiple responses accepted).

In addition, countries mentioned by fewer than one in 10 respondents include:

- 7% export to Pakistan;

- 6% export to each of Indonesia, Malaysia, Vietnam;

- 5% export to each of Bangladesh and Mongolia;

- 4% export to each of Afghanistan and Sri Lanka;

- 3% export to each of Brunei Darussalam and Myanmar; and

- 2% export to each of Cambodia and Laos.

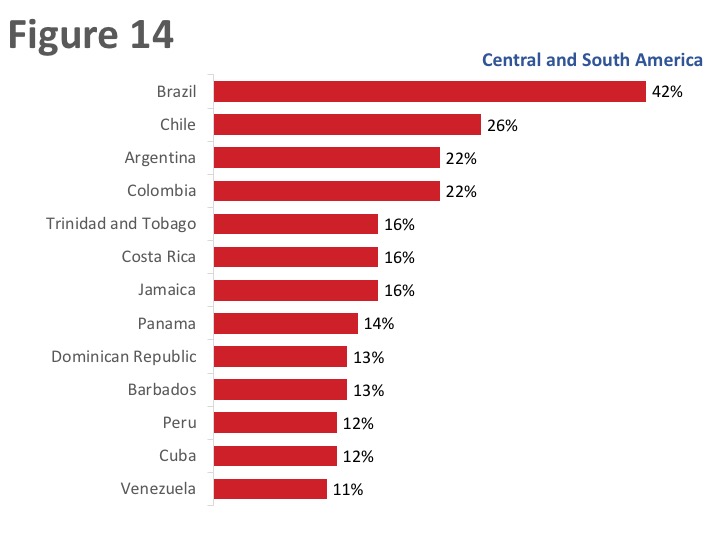

Brazil is the top export destination in Central and South America

Four in 10 (42%) respondents said their company currently exports to Brazil, while 26% export to Chile, 22% to Argentina, and 22% to Colombia. Following this, 16% export to each of Trinidad and Tobago, Costa Rica, and Jamaica. As the graph depicts, smaller proportions of companies export to a variety of other countries in Central and South America.

Figure 14: Current Export Markets: Top Central and South American Destinations

Text Description - Figure 14

Base: n=97; respondents who export to Central and South America. / B2. Which markets does your company currently export to? (multiple responses accepted).

In addition, countries mentioned by fewer than one in 10 respondents include:

- Haiti (9%), Guyana (9%);

- Uruguay (8%), Ecuador (8%);

- Guatemala (7%); and

- Paraguay (6%), El Salvador (6%).

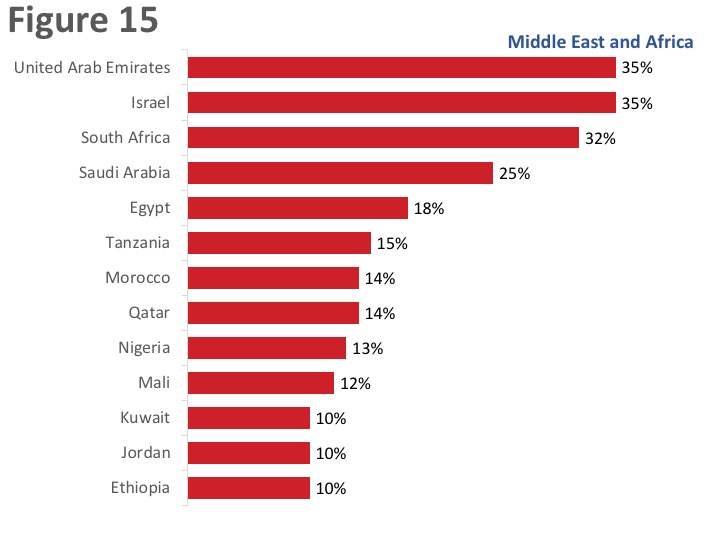

UAE, Israel, and South Africa are top export destinations in Middle East and Africa

Similar proportions said their company currently exports to the United Arab Emirates (UAE) (36%), Israel (35%), and South Africa (32%). Exactly one-quarter (25%) exports to Saudi Arabia and 18% to Egypt. As the graph depicts, smaller proportions of companies export to a variety of other countries in the Middle East and Africa.

Figure 15: Current Export Markets: Top Middle Eastern and African Destinations

Text Description - Figure 15

Base: n=85; respondents who export to the Middle East and Africa. / B3.Which markets, if any, is your company thinking about, or interested in, exporting to? (multiple responses accepted).

In addition, countries mentioned by fewer than one in 10 respondents include:

- Libya (8%), Congo (8%), Sudan (8%), Lebanon (8%), Mozambique (8%);

- Rwanda (7%), Cameroon (7%), Zimbabwe (7%), Cote d'Ivoire (7%);

- West Bank and Gaza Strip (6%), Zambia (6%), Burkina Faso (6%), Senegal (6%); and

- Algeria (5%), Tunisia (5%).

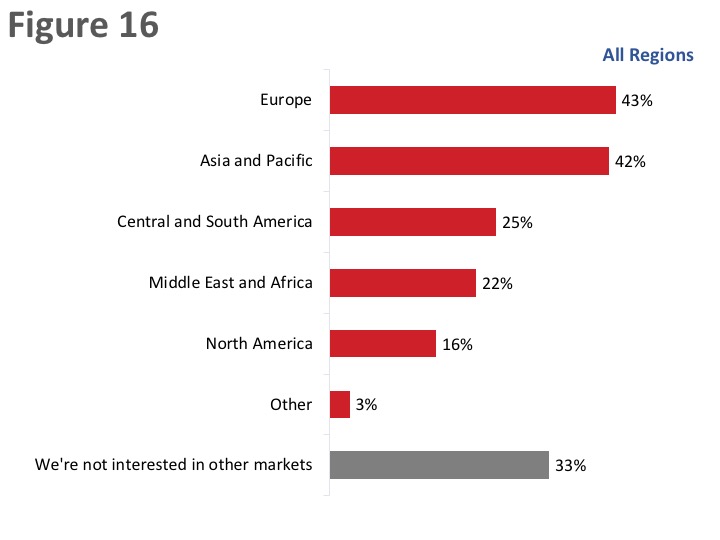

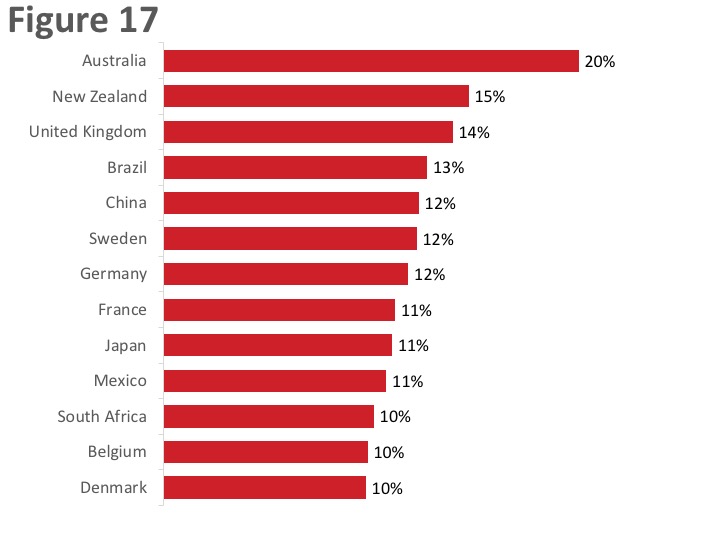

Countries in Europe, Asia and the Pacific are top future destinations of exporters

Asked which markets, if any, their company is thinking about, or interested in, exporting to similar proportions mentioned Europe (43%) and the Asia-Pacific region (42%). Fewer companies are planning to export to countries in Central or South America (25%), the Middle East or Africa (22%), and North America (16%).

One-third of companies are not interested in any other markets at this time.

Figure 16: Future Export Markets

Text Description - Figure 16

Base: n=296; respondents who export goods and services to the US and foreign markets. [Dk/nr: 19%; n=56 removed] / B3. Which markets, if any, is your company thinking about, or interested in, exporting to? (multiple responses accepted).

The top countries identified by respondents as potential export destinations were Australia (20%), followed by New Zealand (15%) and the United Kingdom (14%).

Figure 17: Future Export Markets: Countries

Text Description - Figure 17

Base: n=296; respondents who export goods and services to the US and foreign markets. [Dk/nr: 19%; n=56 removed] / B3.Which markets, if any, is your company thinking about, or interested in, exporting to? (multiple responses accepted).

III. Exporting Obstacles and Assistance

This section presents information about the exporting obstacles encountered by Canadian SMEs, as well as the types of assistance companies would like to help them develop business in markets outside of Canada.

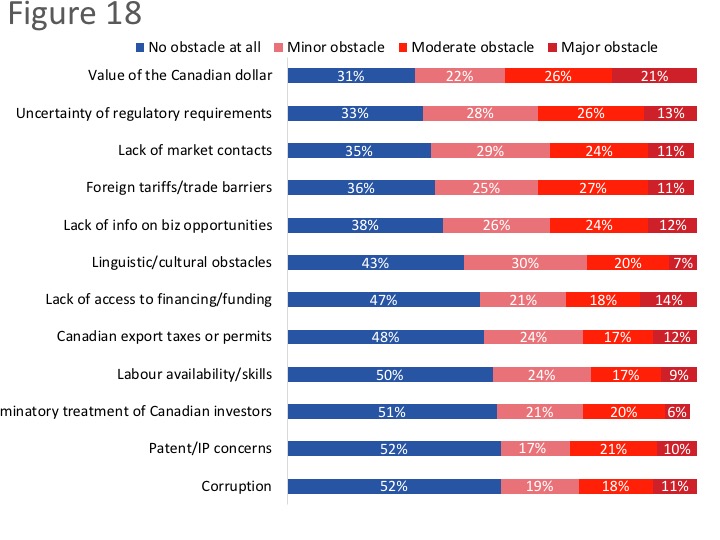

Value of the Canadian dollar is the top challenge experienced by companies

Nearly seven in 10 (69%) reported that the value of the Canadian dollar is at least a minor obstacle to their company’s activities in international markets, including almost half who said it is a moderate (26%) or major (21%) obstacle. At least six in 10 indicated that uncertainty of the regulatory requirements in other countries (67%), lack of market contacts (64%), foreign tariffs and trade barriers (63%), and lack of information on business opportunities (62%) are obstacles for their company. The proportion of respondents rating these as moderate or major obstacles ranged from a low of 36% for lack of information on business opportunities to a high of 39% for tariffs and trade barriers.

In addition, half or more said that linguistic or cultural obstacles (57%), lack of access to financing and funding (53%), and Canadian export taxes or permits (53%) are at least minor challenges for their company when it comes to their company’s activities in international markets.

In contrast, the majority of those surveyed indicated that the following are not challenges faced by their company: corruption (52%), patent/IP concerns (52%), discriminatory treatment of Canadian investors (51%), and labour availability and skills (50%). Respondents who said these issues are challenges for their company were more likely to rate them as minor or moderate obstacles not major obstacles.

Figure 18: Obstacles to Activities in International Markets

Text Description - Figure 18

Base: n=507; all respondents. [Dk/nr: 6%-12%; n= 30-56 removed]. / C2. How large of an obstacle, if at all, are each of the following issues to your company’s activities in international markets?

The value of the Canadian dollar was more likely to be an obstacle for companies planning to export to the Ukraine (90%) than to Mexico or the U.S. (63%). Canadian export taxes or permits were more likely to be an obstacle for companies planning to export to the Ukraine (86%) than to CETA countries (56%). Discriminatory treatment of Canadian investors was more likely to be an obstacle for companies planning to export to the Ukraine (87%) than to Mexico or the U.S. (53%) and CETA countries (52%)[3].

Compared to micro-sized firms (under 5 employees), small companies (5 to 99 employees) were more likely to identify the following as obstacles: the value of the Canadian dollar (74% versus 63%); Canadian export taxes or permits (60% versus 43%); discriminatory/arbitrary treatment of Canadian investors or their investments (54% versus 35%); lack of access to financing or funding (57% versus 46%); foreign tariffs or trade barriers (72% versus 53%); linguistic or cultural obstacles (64% versus 48%); and labour availability and skills (59% versus 37%).

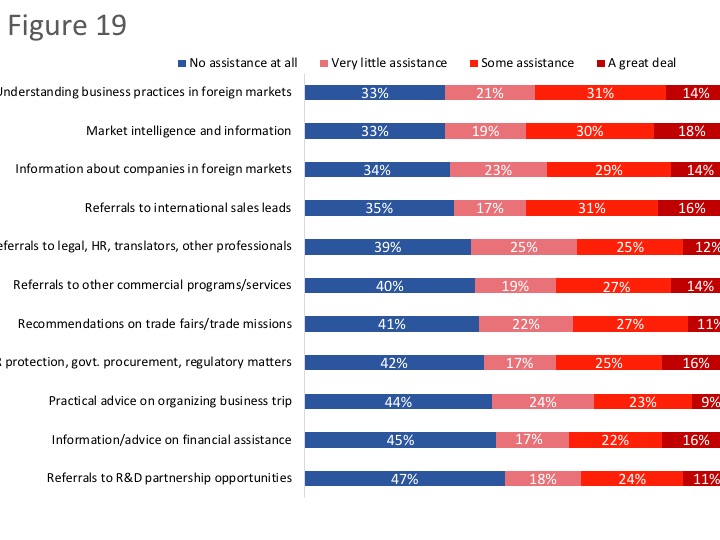

Majority of exporters require at least a little assistance in many areas

Respondents were asked how much assistance, if any, their company needs in the following areas when developing business in markets outside of Canada:

- Market intelligence and information

- Referrals to legal professionals, human resource professionals, translators and other professional service providers

- Support for the protection of intellectual property rights, government procurement and/or regulatory matters

- Referrals to international business opportunities/sales leads

- Referrals of technology and/or R&D partnership opportunities

- Referrals to other relevant commercial programs and services

- Information or advice on locating financial/funding assistance

- Recommendations on trade fairs/trade missions to attend

- Practical advice on timing and organizing your business trip

- Information about organizations or companies in foreign markets

- Understanding responsible business practices in foreign markets.

Areas in which respondents were more likely to say their company requires some or a great deal of assistance include market intelligence and information (48%), referrals to international sales leads (47%), understanding business practices in foreign markets (45%), and information about companies in foreign markets (43%).

Areas in which companies are less likely to require assistance are referrals of technology and/or R&D partnership opportunities (47% of companies require no assistance), information or advice on locating financial/funding assistance financial advice (45% require no assistance), and practical advice on timing and organizing your business trip (44% require no assistance).

Figure 19: Assistance Required to Develop Foreign Markets

Text Description - Figure 19

Base: n= 507; all respondents. [Dk/nr: 6%-9%; n=28-41 removed] / C1. How much assistance, if any, does your company need in the following areas when developing business in markets outside of Canada?

Companies headquartered in western Canada were more likely to not need assistance in many of these areas, including: market intelligence and information; protection of IPR, government procurement and regulatory matters; referrals to international business opportunities/sales leads; referrals to other relevant commercial programs and services; information or advice on locating financial assistance; information about organizations or companies in foreign markets; and understanding responsible business practices in foreign markets.

Micro- and small-sized companies were more likely than medium-sized companies to not need any assistance in these areas.

Compared to companies not planning to export to a country with which Canada has a free trade agreement, companies planning to export to a free trade agreement country were more likely to require assistance in all these areas.

IV. Awareness and Use of Free Trade Agreements

This section presents findings on respondents’ awareness and company use of free trade agreements. At this point in the online questionnaire, respondents were presented with the following information:

Free trade agreements are negotiated to reduce trade barriers, such as import quotas and tariffs, and to increase the trade of goods and services among the participating countries.

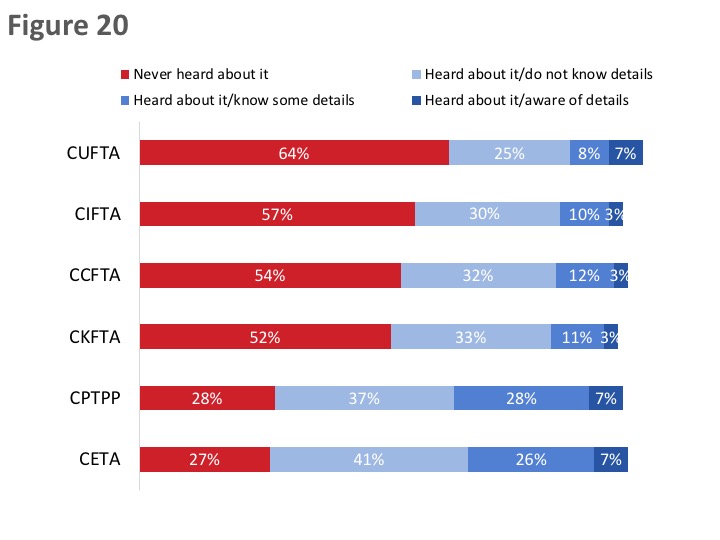

Uneven awareness of free trade agreements

Half or more of respondents have never heard about the following free trade agreements: Canada-Ukraine Free Trade Agreement (CUFTA) (64%), Canada-Israel Free Trade Agreement (CIFTA) (57%), Modernized Canada-Chile Free Trade Agreement (CCFTA) (54%), and Canada-Korea Free Trade Agreement (CKFTA) (52%). Those who claim some awareness of these free trade agreements were more likely to know them by name only (i.e., “heard about it but do not know any details”). Relatively few said they know details about each of these free trade agreements: CUFTA (15%), CIFTA (13%), CCFTA (15%), and CKFTA (14%).

In contrast, there was relatively widespread awareness of the Comprehensive and Progressive Trans-Pacific Partnership (CPTPP) and the Canada-European Union Comprehensive Economic and Trade Agreement (CETA). Seventy-four percent have at least heard about CETA and 72% have at least heard about CPTPP. That said, only 7% of respondents said they are aware of the details of these free trade agreements.

Figure 20: Awareness of Free Trade Agreements

Text Description - Figure 20

Base: n=507; all respondents. / D1. How familiar are you with the following free-trade agreements?

Awareness of all these free trade agreements was higher among medium-sized companies than micro or small companies, and among companies aware of the TCS. In addition, awareness of CKFTA was higher among companies planning to export to a country with which Canada has a free trade agreement (57% versus 42% of those not)

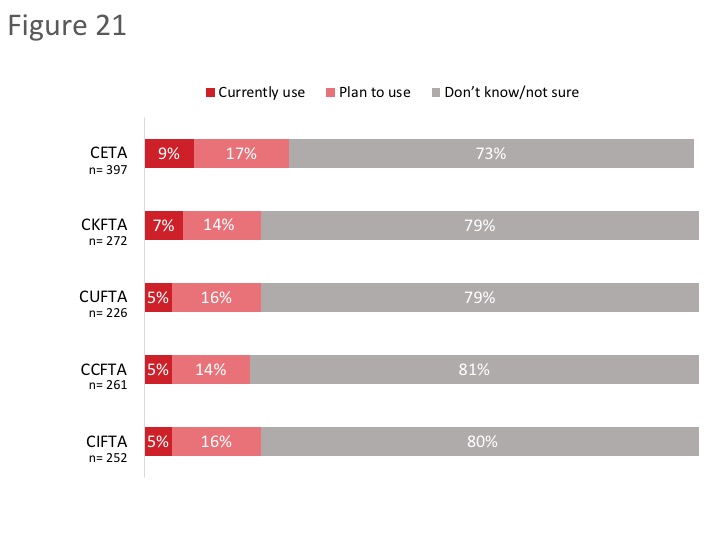

Few companies use any of these free trade agreements

Few companies aware of these free trade agreements are using any of the agreements. Nine percent use CETA and 17% are planning to use this agreement, while 7% use CKFTA and 14% are planning to use the agreement. Five percent of exporting companies aware are using CUFTA, CCFTA, and CIFTA.

Figure 21: Use of Free Trade Agreements

Text Description - Figure 21

Base: those familiar with the FTAs / D2. Does your company currently use or plan to use in the next year any of the following free trade agreements?

Micro-sized companies were less likely than medium-sized companies to be planning to use any of these free trade agreements.

Before being asked about their company’s use of these free trade agreements, respondents were provided with several examples of how their company may be using a free trade agreement. These included:

- claiming preferential tariff treatment for a product their company exports, benefiting from the reduction or elimination of a tariff;

- claiming preferential tariff treatment for an imported product, reducing the cost of their business inputs;

- taking advantage of temporary entry provisions included in an agreement that have facilitated company entry and work authorization in the other country;

- taking advantage of new or enhanced access to government procurement opportunities in a free trade agreement partner country;

- doing business in a free trade agreement partner country in a services sector that has benefitted from improved market access commitments thanks to a free trade agreement; or

- investing in a country with which Canada has a free trade agreement, if the Agreement’s new investment protections influenced the company’s decision to make the investment.

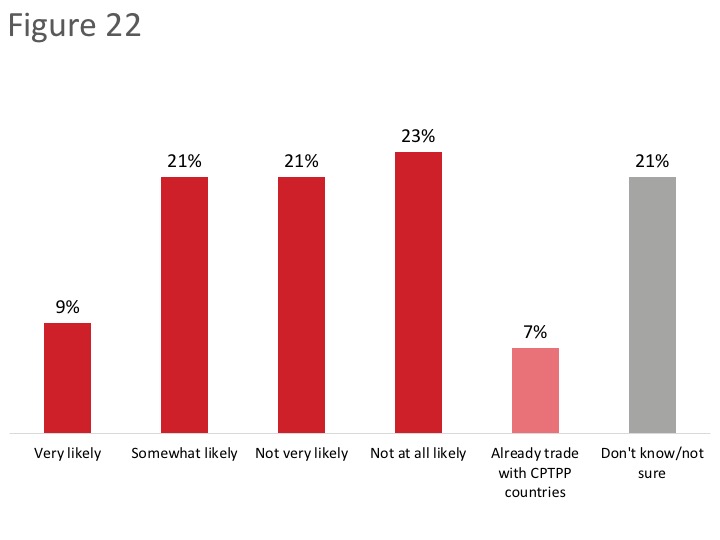

Three in 10 are at least somewhat likely to start trading with CPTPP countries

When asked how likely it is that their company will start to trade with CPTPP countries as a result of this free trade agreement, three in 10 respondents said it is somewhat (21%) or very (9%) likely. Conversely, 21% said it is not very likely and 23% that it is not at all likely that their company will start trading with CPTPP countries. The rest were uncertain (21%) about their company’s plans or indicated that their company already trades with CPTPP countries.

Figure 22: Likelihood of Trading with CPTPP Countries

Text Description - Figure 22

Base: n=507, all respondents. / D3. How likely is it that your company will start to trade with CPTPP countries as a result of this free trade agreement?

Small and medium-sized companies are more likely than micro-sized companies to start to trade with CPTPP countries as a result of this free trade agreement.

Before being asked about their company’s use of the CPTPP, respondents were provided with the following information about the agreements:

The Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP) is a free trade agreement between Canada and 10 other countries in the Asia-Pacific region: Australia, Brunei, Chile, Japan, Malaysia, Mexico, New Zealand, Peru, Singapore, and Vietnam. Once the agreement is fully implemented, 99% of all tariff lines will be duty-free. The CPTPP also provides exporters with enhanced access to government procurement opportunities in CPTPP markets, offers greater certainty and stability for investors and companies in the service sectors, and increases labour mobility.

On December 30, 2018 the CPTPP entered into force among the first six countries to ratify the agreement – Canada, Australia, Japan, Mexico, New Zealand, and Singapore. On January 14, 2019, the CPTPP entered into force for Vietnam. Peru, Chile, Malaysia, and Brunei have not yet ratified the Agreement.

Virtually all companies that currently trade with CPTPP countries (n=30)[4] are likely to continue trading with these countries as a result of the trade agreement (88% are very likely and 9% are somewhat likely). The rest (3%) were uncertain about their company’s plans.

Over the next three years, the majority of these respondents (n=30)[5] expect their company’s volume of exports to the Asia-Pacific region will stay about the same (51%). Among those who expect a change, just over one-quarter expect export volumes to increase somewhat (24%) or significantly (3%). One in 10 expect export volumes to decrease somewhat and the rest (12%) do not know what to export in terms of the outlook for export volumes to the Asia-Pacific region.

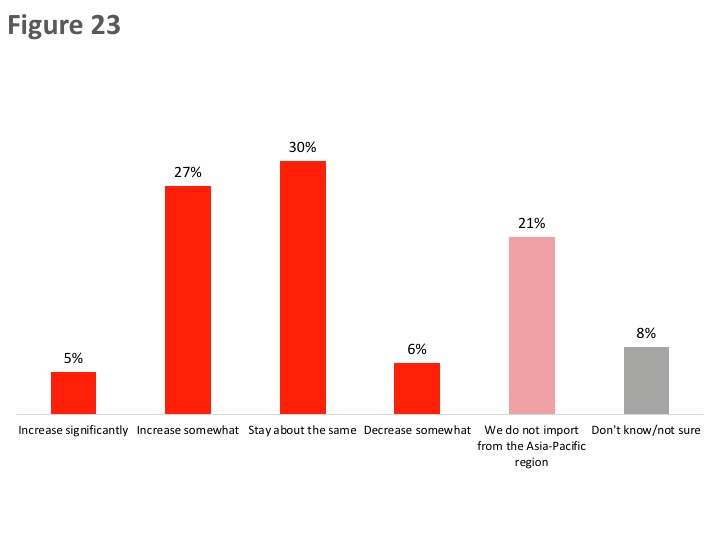

Importers do not expect a decrease in the volume of imports from Asia-Pacific region

Almost one-third (32%) of importers expect the volume of imports from the Asia-Pacific region to increase somewhat (27%) or significantly (5%). Almost as many (30%) export the level of imports to remain the same. Only 6% anticipate a decrease (8% were uncertain about the outlook and 21% do not import from this region).

Figure 23: Outlook for Import Volumes from the Asia-Pacific Region

Text Description - Figure 23

Base: n=215; companies that import / D6. Over the next three years, do you expect the volume of your company’s imports from the Asia-Pacific region will …?

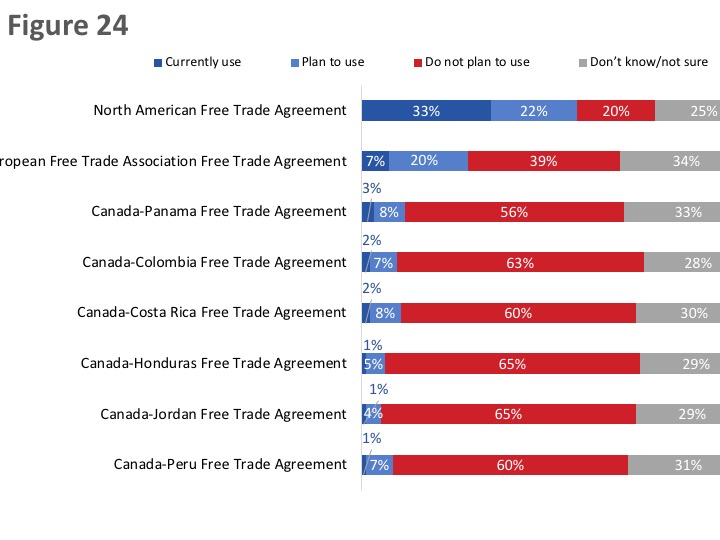

Companies most likely to be using or planning to use NAFTA

One-third (33%) of respondents said their company currently uses the North American Free Trade Agreement (NAFTA) and 22% said their company is planning to start using the agreement in the next year. In total, therefore, 55% of companies are currently or planning to use NAFTA. The rest reported that their company has no plans to use NAFTA (20%) or that they are uncertain of their company’s plan in relation to this trade agreement (25%). Following NAFTA, 7% of companies are using the Canada-European Free Trade Association Free Trade Agreement and 20% are planning to use the agreement in the next year.

The majority of companies are not using and have no plans to use the following free trade agreements: Canada-Honduras Free Trade Agreement (65%), Canada-Jordan Free Trade Agreement (65%), Canada-Colombia Free Trade Agreement (63%), Canada-Peru Free Trade Agreement (60%), Canada-Costa Rica Free Trade Agreement (60%), and Canada-Panama Free Trade Agreement (56%).

Figure 24: Use of other free trade agreements

Text Description - Figure 24

Base: n=507; all respondents. / D7. Which, if any, other free trade agreements does your company currently use or plan to start using in the next year?

Micro- and small-sized companies are more likely than medium-sized companies to not be planning to use any of the free trade agreements. Companies planning to start exporting to countries with which Canada has a free trade agreement were more likely than those that are not to be planning to use one of these free trade agreements.

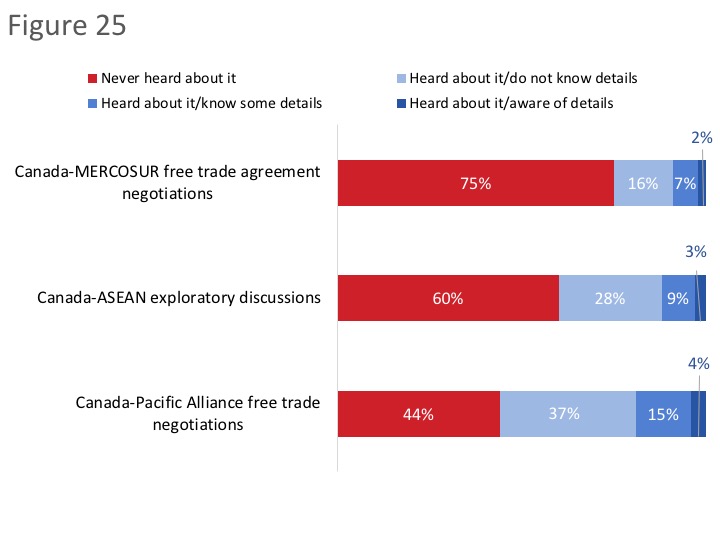

Limited awareness of specific free trade agreement negotiations or discussions

Three-quarters (75%) of respondents have not heard about the Canada-MERCOSUR free trade agreement negotiations. Those who have are more likely to know these negotiations by name only (16%) than to know some (7%) or all (2%) details. In addition, 60% are not aware of the Canada-ASEAN exploratory discussions. Of those who are aware, 28% have heard about the exploratory discussions, 9% know some details, and 3% are aware of the details of these discussions.

Awareness of the Canada-Pacific Alliance free trade negotiations is somewhat higher, with only 44% of respondents saying they have not heard about these negotiations. Of those who are aware, 37% have heard about the free trade negotiations, 15% know some details, and 4% are aware of the details. In total, therefore, 56% of respondents are aware of the Canada-Pacific Alliance free trade negotiations at least by name.

Figure 25: Awareness of free trade discussions or negotiations

Text Description - Figure 25

Base: n=507; all respondents. / D8. Have you heard anything about the following free trade agreement negotiations or discussions?

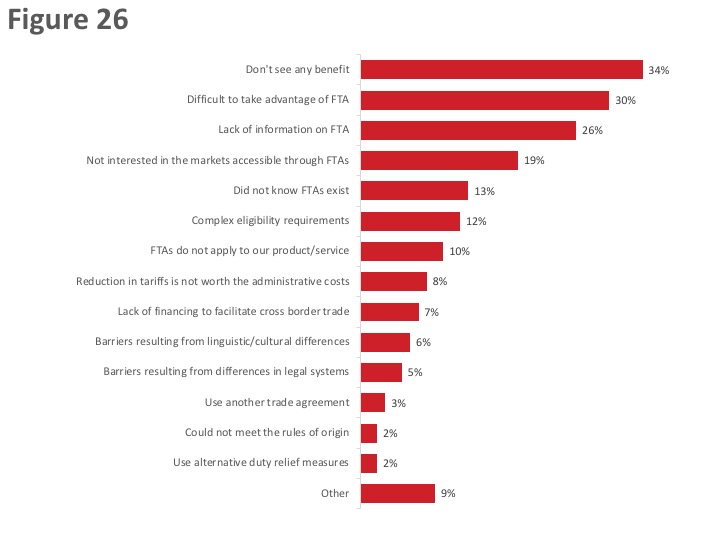

Various reasons for not using free trade agreements

Respondents who indicated that their company is not using free trade agreements to export goods or services (n=272) pointed to a variety of reasons to explain why this is the case. Topping the list, however, were the perceptions that there is no benefit for their company to be derived from using a free trade agreement (34%) and that free trade agreements are difficult to take advantage of/to use (30%). Following this, one-quarter (26%) said their company lacks information on free trade agreements and almost one in five (19%) mentioned that their company is not interested in the markets accessible through Canada’s free trade agreements.

Reasons mentioned by approximately one in 10 included lack of awareness of Canada’s free trade agreements (13%) as well as the perceptions that the eligibility requirements are complex (12%) or that the agreements do not apply to the company’s products or services (10%).

As depicted in the graph, a variety of other reasons were offered to explain why their company is not using any of Canada’s free trade agreements by fewer than one in 10 respondents.

Figure 26: Reasons for Not Using Free Trade Agreements

Text Description - Figure 26

Base: n=272; those who do not use FTAs. [Dk/nr: 2%; n=5 removed] / E1. Why is your company not using free trade agreements to export goods or services? (multiple responses accepted).

V. Impact of Free Trade Agreements

This section presents findings on the perceived impact of free trade agreements on Canadian SMEs. These questions were only asked of respondents who indicated that their company uses one or more free trade agreements.

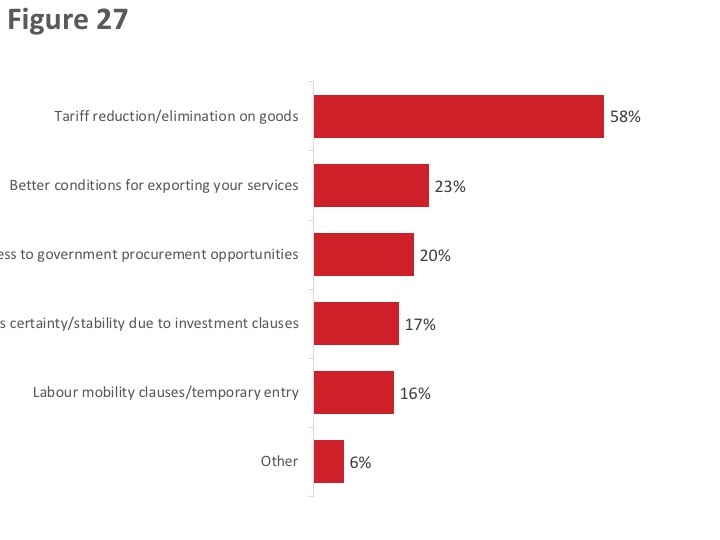

Tariff reduction is the top perceived benefit of using free trade agreements

Nearly six in 10 (58%) companies that use free trade agreements (n=191) have benefited from tariff reduction or elimination on goods. Significantly fewer have benefitted from better conditions for exporting their services (23%), easier access to government procurement opportunities (20%), greater business certainty/stability due to investment clauses in the agreement (17%), and labour mobility clauses/temporary entry (16%).

Figure 27: Benefits of Using Free Trade Agreements

Text Description - Figure 27

Base: n=191; those who use FTAs. [Dk/nr: 9%; n=18 removed] / E2. Thinking about the free trade agreements that your company currently uses, has your company benefited from any of the following? (multiple responses accepted).

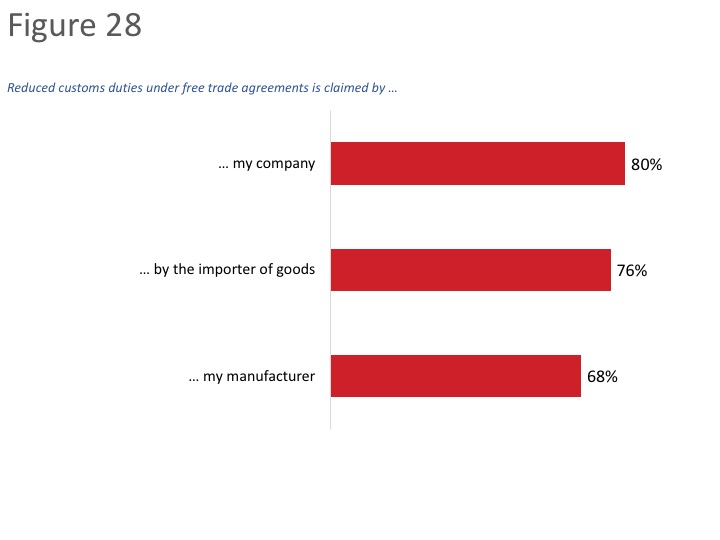

Company, followed by the importer are more likely to claim reduced customs duties

Among companies that have benefited from tariff reduction or elimination on goods (n=121), 80% claimed the reduced customs duties under the free trade agreements they use. Alternatively, 76% said this was claimed by the importer of the goods, and 68% by the manufacturer.

Figure 28: Customs Duties

Text Description - Figure 28

Base: n=121; those who benefited from tariff reduction. [Dk/nr: 74%-96%; n=46-48 removed] [Not applicable: 10%-21%; n= 5-11 removed] / E3. Did your company, your manufacturer or the importer of your goods claim reduced customs duties under a free trade agreement?

Various factors influenced companies’ decision to not claim the reduced customs duties

Respondents who indicated that their company did not claim the reduced customs duties (n=52) were asked what impact, if any, a number of factors had on the decision. The factors included:

- The good we export is not covered by the free trade agreement.

- We did not see a significant tariff reduction as a result of the free trade agreement.

- We did not know we needed to apply for a free trade agreement preference.

- We do not understand free trade agreements or the eligibility requirements/rules of origin.

- The delays associated with obtaining Origin Declarations are too long.

- The administrative costs associated with obtaining Origin Declarations are too high.

- We use the tariff preferences available under the World Trade Organization (WTO) because the rules/requirements are simpler.

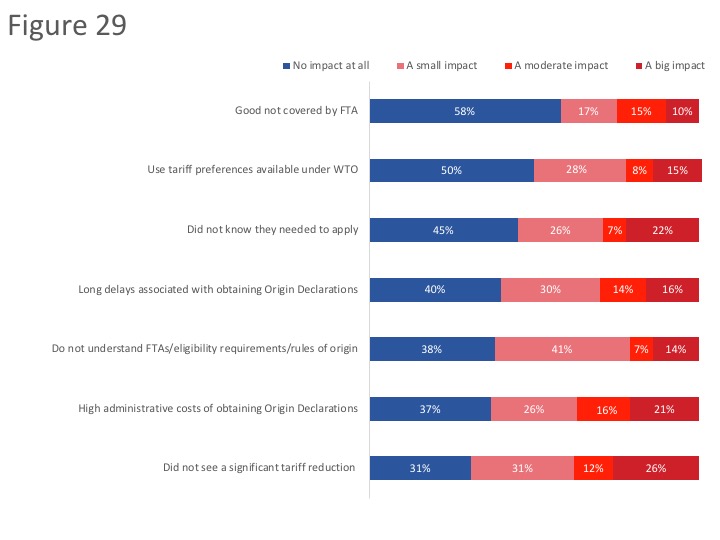

Respondents were more likely to point to the following as factors as having at least a small impact on their company’s decision: not seeing a significant tariff reduction (66% including 26% who said this had a big impact), high administrative costs of obtaining Origin Declarations (63%), lack of understanding of free trade agreements, eligibility requirements or rules of origin (62%), and long delays associated with obtaining Origin Declarations (60%).

The majority of respondents said that their good not being covered by the free trade agreement (58%) and use of tariff preferences available under the WTO (50%) had no impact on their company’s decision to not claim reduced customs duties.

Figure 29: Reasons for Not Claiming Reduced Customs Duties

Text Description - Figure 29

Base: n=52; those who did not claim reduced custom duties. [Dk/nr: 22%-47%; n=9-16 removed] / E4. What impact, if any, did the following factors have on your company’s decision to not claim reduced customs duties for your goods?

Impact of free trade agreements on government procurement not known

Respondents who indicated that their company has benefited from easier access to government procurement opportunities (n=61) were asked to rate their level of agreement or disagreement with the following:

As a result of free trade agreements…

- Our company has better access to information regarding foreign government procurement opportunities.

- Our company is pursuing foreign government procurement contracts in free trade agreement partner countries.

- Our company has been able to more easily apply for foreign government procurement opportunities.

- The foreign government procurement process fairly lets Canadian companies compete against local businesses.

In all cases, the majority of respondents indicated that they did not know what impact free trade agreements have had in these areas.

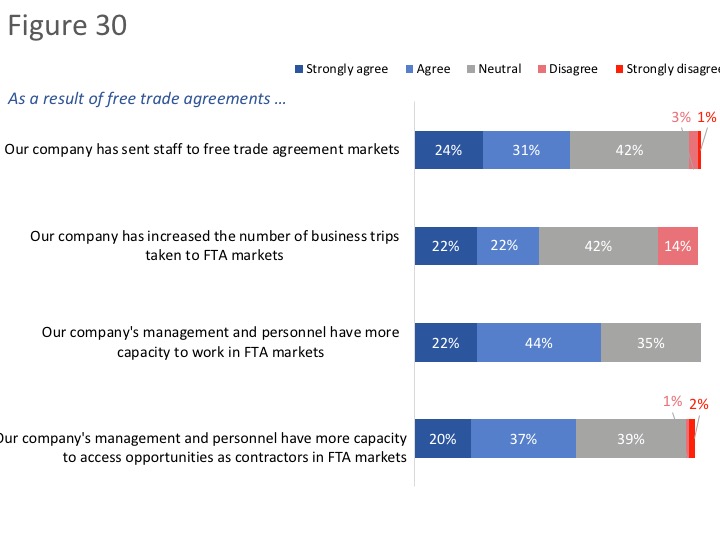

Various impacts of free trade agreements on labour mobility

Respondents who indicated that their company has benefited from labour mobility or temporary entry clauses (n=47) were most likely to agree that their company’s management and personnel have more capacity to work in free trade agreement markets (66%) as a result of free trade agreements. In addition, more than half agreed that their company’s management and personnel have more capacity to access opportunities as contractors in free trade agreement markets (57%) and have sent staff to free trade agreement markets (55%). Respondents were less likely to report that their company has increased the number of business trips taken to free trade agreement markets (44%).

Figure 30: Impact of free trade agreements on labour mobility

Text Description - Figure 30

Base: n=47; those who used labour mobility or temporary entry clauses. [Dk/nr: 37%-45%; n=10-12 removed] / E6. How much do you agree or disagree with the following statements?

Free trade agreements have modest impact on business practices

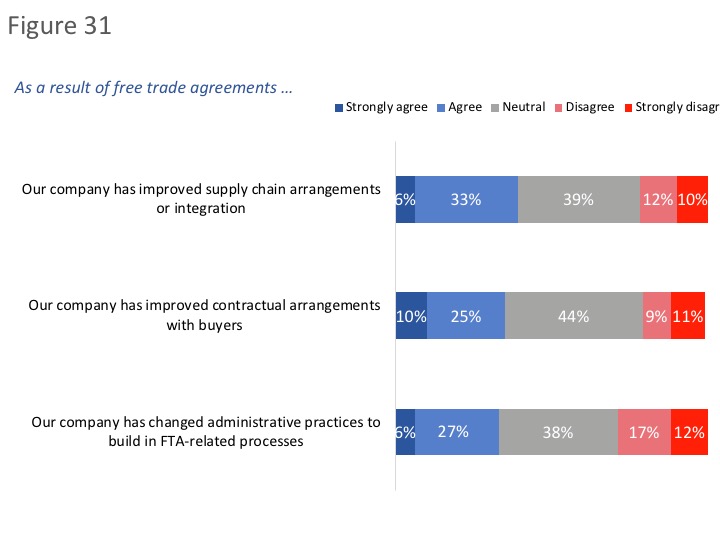

Those who said their company uses free trade agreements (n=191) were asked about the impact of these agreements on their company’s business practices.

Nearly four in 10 (39%) agreed that free trade agreements have improved their company’s supply chain arrangements or integration, while 22% disagreed. The rest (39%) were neutral, neither agreeing nor disagreeing that their company has improved supply change arrangements or integration.

Following this, 35% agreed that their company has improved contractual arrangements with buys, and 33% that their company has changed administrative practices to build FTA-related processes. Those who did not agree were more likely to be neutral than to express disagreement.

Figure 31: Impact of free trade agreements on business practices

Text Description - Figure 31

Base: n=191; those who used FTAs. [Dk/nr: 37%-45%; n=10-12 removed] / E7. How much do you agree or disagree with the following statements?

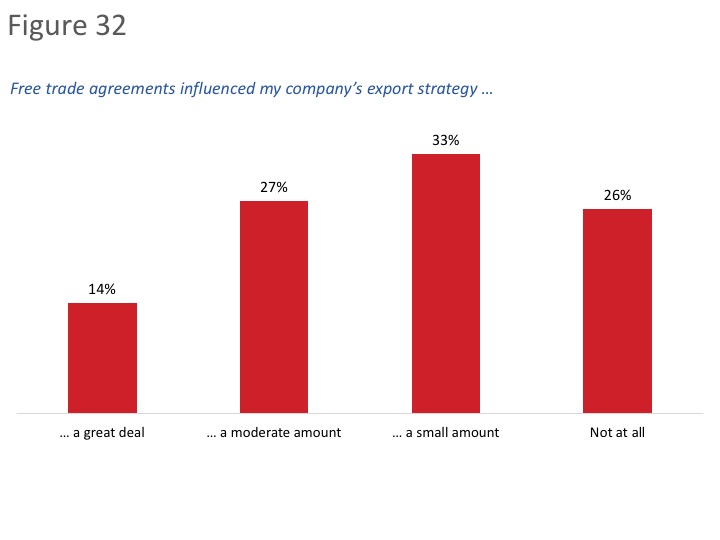

Free trade agreements influence companies’ export strategy in various ways

Most respondents said free trade agreements influence their company’s export strategy at least a small amount. Specifically, 14% are influenced a great deal by free trade agreements, 27% a moderate amount, and 33% a small amount. Conversely, the export strategy of one-quarter (26%) of companies is not at all influenced by Canada’s free trade agreements.

Figure 32: Influence of free trade agreements on export strategy

Text Description - Figure 32

Base: n=235; those aware of FTAs. [Dk/nr: 5%; n=9 removed] / E8. How much, if at all, do free trade agreements influence your company’s export strategy and encourage you to consider new markets?

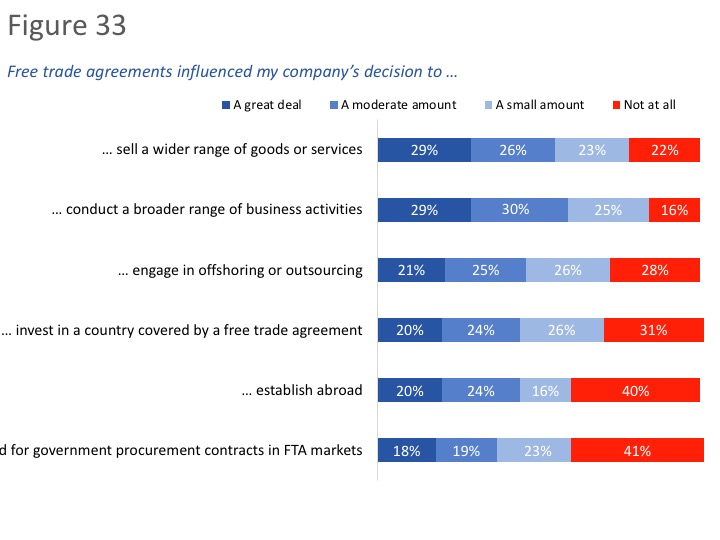

Companies are influenced by free trade agreements in various ways. Most (84%) respondents said that free trade agreements have influenced their company’s decision to conduct a broader range of business activities, including 29% who said it influenced their company a great deal. In addition, nearly eight in 10 (78%) reported that free trade agreements have influenced their company’s decision to sell a wider range of goods or services, while seven in 10 said these agreements encouraged their company to engage in offshoring or outsourcing (72%) or to invest in a country covered by a free trade agreement (70%).

Free trade agreements were less likely to have influenced companies to establish abroad or to bid for government procurement contracts in free trade agreement markets. The plurality (40% and 41%, respectively) reported that free trade agreements did not at all influence their company’s decision to engage in these activities.

Figure 33: Areas in which free trade agreements influenced export strategy

Text Description - Figure 33

Base: n191; those who’s export strategy was influenced by FTAs. [Dk/nr: 4%-8%; n=6-10 removed] [Does not apply: 7%-26%; n=10-30 removed] E9. How much, if at all, have free trade agreements influenced your company’s decision to…?

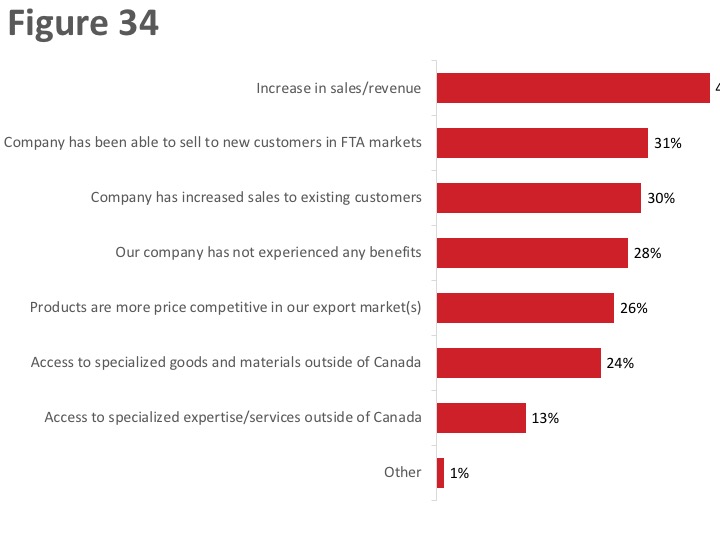

Other benefits of free trade agreements include increased sales and customer acquisition

When asked what other benefits, if any, their company has experience as a result of using free trade agreements, 40% of respondents pointed to increased sales or revenues, 31% to the acquisition of new customers in free trade agreement markets, and 30% to increased sales to existing customers.

In addition, approximately one-quarter mentioned that products are more price competitive of their export markets (26%) and that their company is able to access specialized and goods and materials outside of Canada (24%). Thirteen percent said their company has benefited from access to specialized expertise and services outside of Canada as a result of free trade agreements.

Nearly three in 10 (28%) said their company has not experienced any benefits of free trade agreements.

Figure 34: Other benefits of free trade agreements

Text Description - Figure 34

Base: n=235; those aware of FTAs. [Dk/nr: 1%; n=1 removed] / E10. What other benefits, if any, has your company experienced as a result of using free trade agreements?

VI. Awareness of the Trade Commissioner Service

This section presents findings on respondents’ awareness and perceptions of the Trade Commissioner Service (TCS). These questions were only asked of respondents aware one or more free trade agreement.

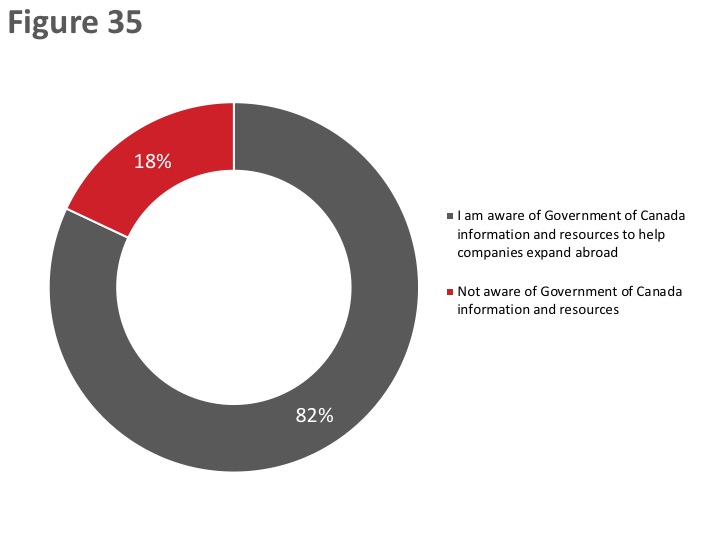

Widespread awareness of Government of Canada information and resources for exporters

Eight in 10 (82%) respondents aware of free trade agreements (n=235) indicated that they are aware that the Government of Canada has information and resource available to help companies their business abroad. Conversely, 18% are not aware.

Figure 35: Awareness of GoC resources and information

Text Description - Figure 35

Base: n=235; those aware of FTAs / F1. Are you aware that the Government of Canada has information and resources available to help companies expand their business abroad?

Awareness that the Government of Canada has information and resources available help companies expand their business abroad was higher among those aware of the TCS (94% versus 69% of those not aware), micro-sized firms (95% versus 74% of small firms and 78% of medium-sized firms) and firms currently exporting to the U.S. and foreign markets (86% versus 70% of those exporting only to the U.S.),

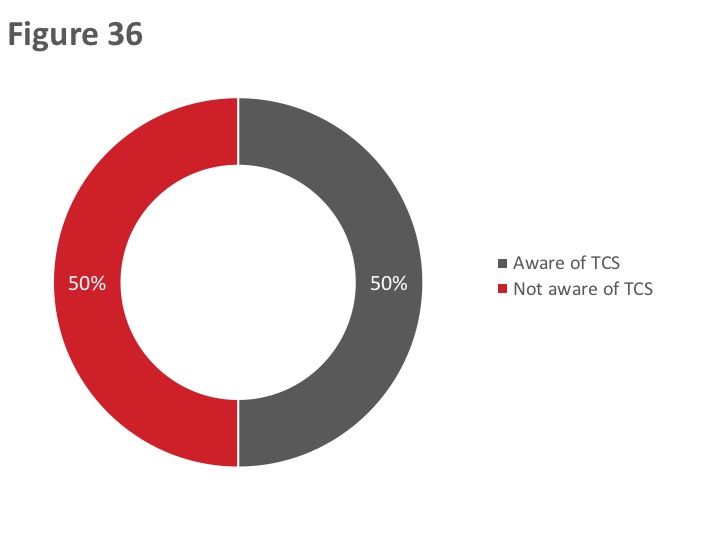

Half aware of the TCS; most of those aware know of the TCS by name only

Exactly half (50%) of those aware of free trade agreements have heard of the Trade Commissioner Service, or TCS.[6] Those aware of the TCS (n=115) were asked what, if anything, they have heard about it. Most (83%) acknowledged that they had heard of the TCS, but that they could not recall anything specific about the TCS. Beyond this, 13% had heard that the TCS provides trade assistance.

Figure 36: Awareness of TCS

Text Description - Figure 36

Base: n=235; those aware of FTAs / F2. Have you ever heard of the Trade Commissioner Service, or TCS?

Four in 10 first learned about the TCS via the internet

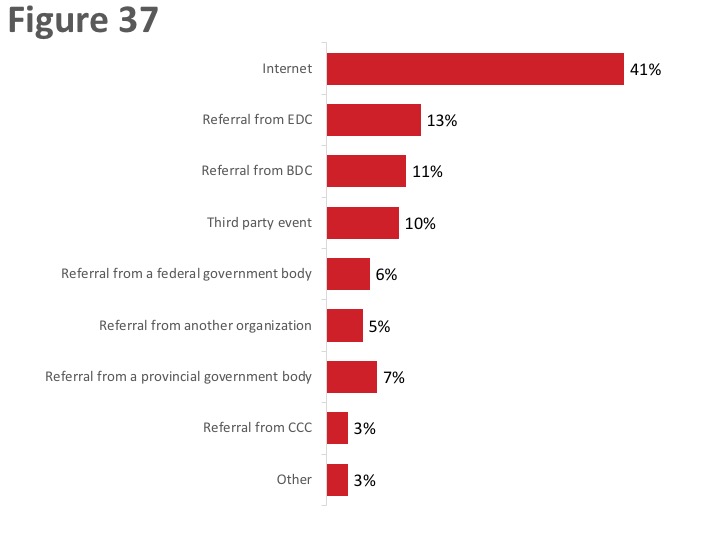

Those aware of the TCS were most likely to have initially learned about the TCS through the internet (40%). Following this, a small number of respondents mentioned a referral from Export Development Canada (EDC) (13%) or the Business Development Bank of Canada (BDC) (11%) and via a third-party event (10%). All other sources of awareness were mentioned by fewer than one in 10.

Figure 37: Source of Awareness of TCS

Text Description - Figure 37

Base: n=116; those aware of TCS. [Dk/nr: 14%; n=13 removed] / F4. How did you initially learn about the Trade Commissioner Service (or TCS)?

VII. Communication Preferences and Information Needs

This section presents findings on respondents’ communication preferences and information needs.

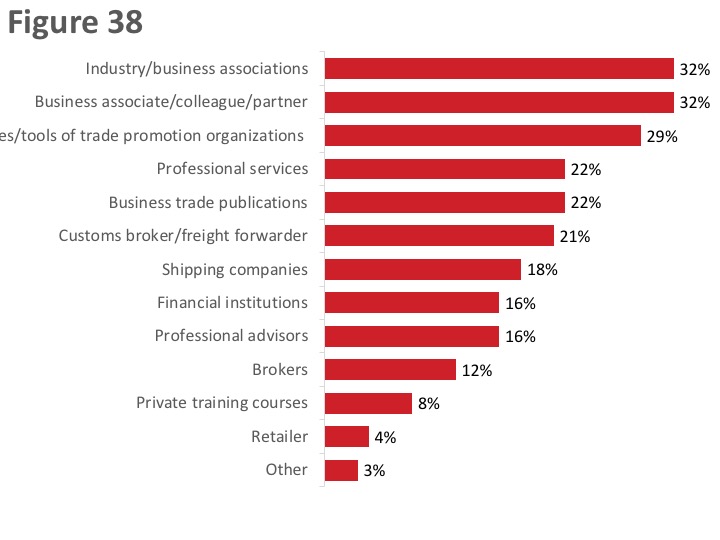

Top information sources for doing business abroad – associations and colleagues

When asked where they get their information and advice on doing business abroad, such as exporting and using free trade agreements, approximately one-third each mentioned industry or business associations (32%) and business associates, colleagues, or partners (32%).

Twenty-nine percent use the websites or free online tools of trade promotion organizations. Respondents who use the information and resources of trade promotion organizations (n=49) were most likely to mention BDC (50%), followed at a distance by EDC (38%), provincial export organizations (26%), and the Trade Commissioner Service (20%).

Approximately two in 10 use professional services (22%), business trade publications (22%), and customs brokers/freight forwarders (21%), while smaller proportions rely on shipping companies (18%), financial institutions (16%), professional advisors (12%), brokers (12%), private training courses (8%), and retailers (4%) for information and advice on doing business abroad.

Figure 38: Information Sources for Doing Business Abroad

Text Description - Figure 38

Base: n=507; all respondents. [Dk/nr: 5%, n=22 removed] / G1. Where do you get your information and advice on doing business abroad (i.e., exporting and/or using free trade agreements)? (multiple responses accepted)

The likelihood of using industry and business associations was higher among companies that currently export to free agreement countries (34% versus 17%) and among those aware of the TCS (50% versus 25% of those not aware). The likelihood of using a business associate or colleague was higher among companies in western Canada (32%) and Ontario (36%) compared to those in Quebec (18%), those aware of the TCS (44% versus 23%), and those companies that export services only (38% compared to 30% of those that export goods and services).

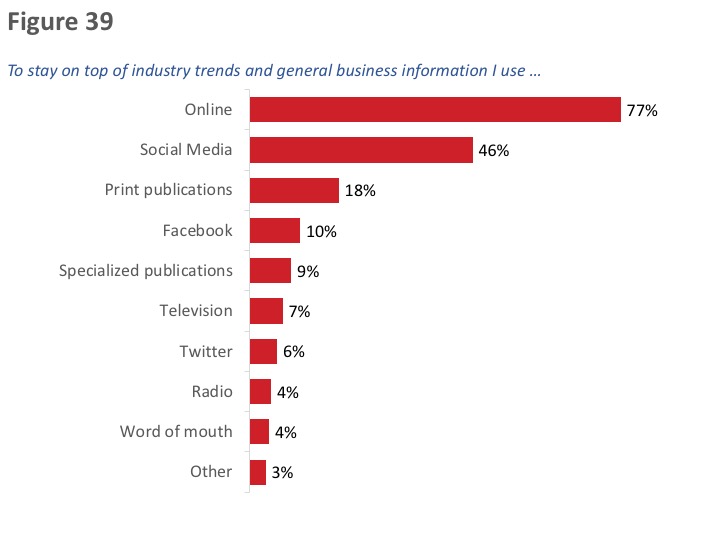

Vast majority uses the internet to stay on top of industry trends and general business information

Just over three-quarters (77%) of respondents said they look to the internet when it comes to staying on top of industry trends and general business information. Following this, 46% use social media. Other sources were used by fewer than two in 10.

Figure 39: Information Sources Used to Stay on Top of Industry Trends

Text Description - Figure 39

Base: n=507; all respondents. [Dk/nr: 4%; n=19 removed]. / G2. When it comes to staying on top of industry trends and general business information, where do you typically look? (multiple responses accepted).

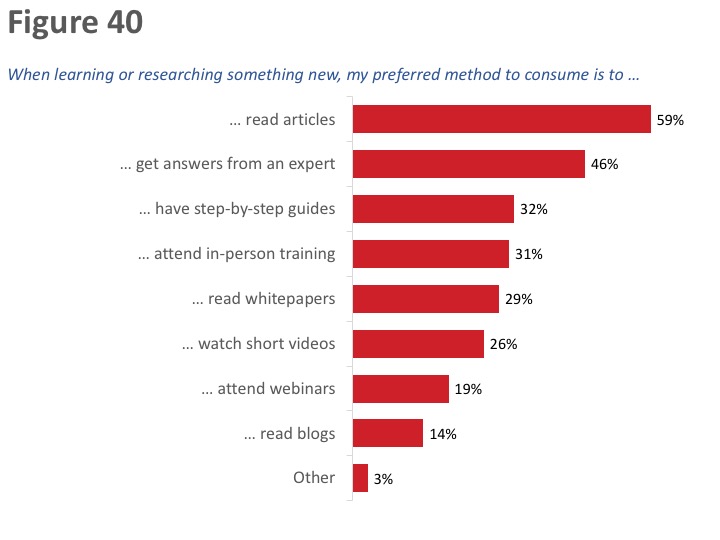

Reading articles, getting answers from experts – top methods to consume information

When learning or researching something new, 59% of respondents prefer to read articles and 46% to get answers from an expert. Approximately one-third each expressed a preference for step-by-step guides (32%) and in-person training (31%), while 29% would like to read whitepapers and 26% would prefer to watch short videos. Following this, 19% prefer to attend webinars and 14% to read blogs.

Figure 40: Preferred Methods to Consume information

Text Description - Figure 40

Base: n=507; all respondents. [Dk/nr: 1%, n=4 removed] / G3. How do you prefer to consume information when learning or researching something new? (multiple responses accepted)

Those who prefer to get their answers from an expert, from in-person training, and from attending webinars were more likely to be aware of the TCS. The likelihood of preferring to get answers from an expert was higher among respondents representing companies planning to start export exporting to countries with which Canada has free trade agreements.

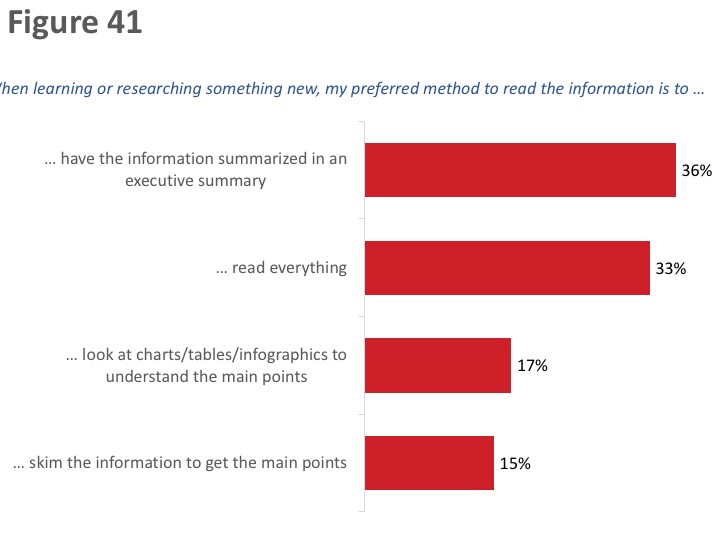

No consensus on preferred methods to read information

Approximately one-third each prefer to have information summarized in an executive summary (36%) or to read everything (33%), while 17% prefer charts, tables, or infographics and 15% skim the information to get the main points.

Figure 41: Preferred Methods to Read information

Text Description - Figure 41

Base: n=507; all respondents. / G4. Which of the following best describes how you prefer to read information?

Those who prefer to read everything were more likely to represent micro-sized firms and companies operating in the information and cultural industries (compared to those active in the manufacturing sector).

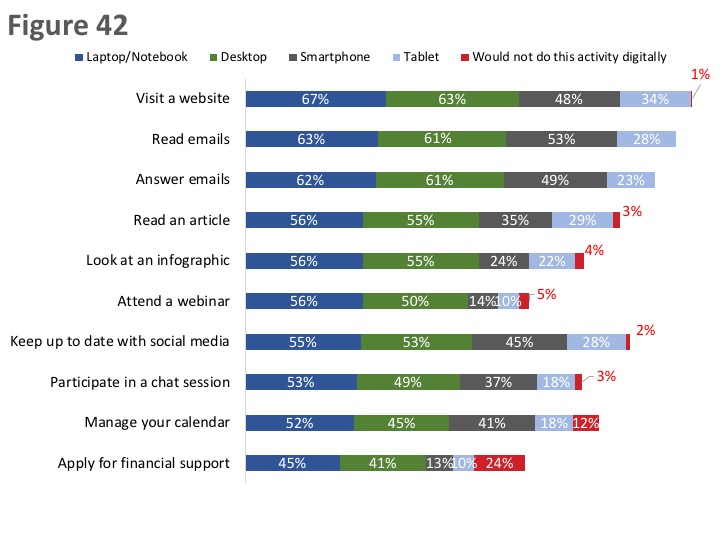

Laptop/desktops preferred to mobile devices for most business tasks

As the graph below depicts, the vast majority of respondents would do all these tasks or activities digitally.

Figure 42: Preferred Device for Various Activities

Text Description - Figure 42

Base: n=507; all respondents. [I don’t do this activity: <0.5%-40%, n=2-144 removed] / G5. On which device would you do each of the following activities? You can choose more than one device for each activity .(multiple responses accepted).

When researching something new, most would start online and then determine next steps

Respondents were asked which of the following descriptions best describes how they would research something new:

- I would call someone first to help me figure out where to look for new information and then I would search for it in a specific place online. I would probably want to have someone to talk to after I found the information just to make sure I have the right information

- I would start searching online for the information I am looking for, sifting through all of the available sources and then making a decision about what my next step is based on everything I learned.

- I would only look at information if it came through my inbox first. I would only go online to search something if the email or subscription caught my attention.

- I would ask someone in my company to research the information for me and present me with their findings

Figure 43: Approach to Researching Something New

Text Description - Figure 43

Base: n= 507; all respondents. / G6. Please choose the option that best describes how you would research something new.

When researching something new, 83% of respondents would start searching online, and then make a decision about what the next step would be based on everything learned. Relatively few would call someone to figure out where to look before searching online (12%), would first only look at information in their inbox (3%), and would ask someone to research the information and present the findings (2%).

Phase 2: In-depth Interviews

I. Context

This section provides background information on participants and their companies’ involvement in international business activities.

Participants’ positions/titles

Participants in this study occupy various positions in their respective companies. Types of job titles held by participants included the following: Owner, President, Chief Executive Officer, Chief Financial Officer, Chief Operating Officer, Chief Accountant, Director of Operations, Chief Designer, General Manager, Manager of Purchasing and Shipping, Sales Manager, Procurement Manager, Sales Executive.

Nature of companies’ international business activities

Types of activities companies engage in as part of their current international business include the following:

- Exporting goods: Examples of goods exported by participants’ companies include steel products, hydraulic cylinders, products related to the hospitality industry, parts for oil wells, automotive parts, cement, valves and pumps, emission combustors, waste water treatment products, machine parts, vehicular electronic products, books/publications, medical products, dry goods, health food products, meat products (specifically pork-based products), software products, custom clothing, cosmetic products, semi-finished products, pet food products, leather goods, jewelry, and horses and equipment for horses.

- Exporting services: Examples of services offered by participants’ companies as part of their international business include web design and development, electronic products design services, legal services, auditing services, consulting services, technical training, online publication services, and marketing-related services.

- Exporting goods and services: Some participants said their companies engage in the export of both goods and services. Examples include exporting products as well as upgrading and servicing them on the ground, offering consulting services as well as manufacturing/exporting goods, exporting products as well as training technicians on the ground, and exporting products as well as installing them on the ground.

- Importing goods, as well as sourcing and importing components as part of a supply/value chain: Some participants said their companies import goods or source/import components or materials as part of a supply or value chain (e.g., importing food products, importing diamonds and other types of gems for the production of jewelry, importing nuts and bolts as components for the production of machinery).

- Presence/involvement in other countries: Some participants specified that they have a presence or involvement in other countries. This includes distribution centers in various locations (e.g., warehouses), employing personnel in other countries (e.g., software developers), and on location/on the ground production (e.g., manufacturing dry goods).

Countries or regions where companies are active

Participants collectively identified numerous countries and/or regions in which their companies are currently active in terms of international business, but the United States (U.S.) followed by Europe/the European Union were most often identified as current markets. Beyond the U.S. and Europe, a variety of specific countries/regions were mentioned by participants.

Figure 44: Companies or regions where companies are active

Text Description - Figure 44

Most participants whose company operates in more than one country or region described their activities as similar or the same (i.e., they undertake the same or similar types of activities in the various regions in which they currently operate). To the extent that there were differences, these differences tended to relate to approaches and strategies as opposed to actual types of activities. For example, some participants said they use different approaches or strategies for marketing their products in different regions, based on various factors (e.g., the nature of their target market, cultural factors, the advice of sales representatives, the availability of distributors and consultants on the ground, their general familiarity with the country or market).

China was occasionally identified specifically as a market in which a different approach is used, given cultural differences between China and the West, as well as the size and diversity of the market (i.e., it can differ from region to region).

Some said their approach or strategy tends to be ‘ad hoc’ or circumstantial (e.g., it depends on who their partners, collaborators/intermediaries, and clients are in various countries). In other words, one adapts one’s approach based on specific circumstances, including the needs, requirements, and preferences of clients and partners. By contrast, authors/novelists who sell and promote their products online (e.g., through Amazon), as well some service providers, said their activities tend to be homogeneous regardless of the market in which they operate.

Length of time companies have been involved in international business

Not surprisingly, there was no consistency or uniformity in terms of how long companies have been involved in international business. Indeed, involvement varied from as recently as the last year to as long as 40 years. That said, most participants said their company has been involved in international business for at least five years.

Some companies began with international focus while most others began with domestic focus

Once again, perhaps not surprisingly, there was no uniformity in terms of how companies got involved in international trade in the first place. That being said, most indicated that their company began with a domestic focus and then later developed an international focus. While there was no uniform path or avenue from the domestic to the international market, certain ‘circumstantial’ factors (and variations on them) were routinely provided to explain the evolution. Such reasons included the following:

- Possibilities arising as a result of connections, networking, and contracting opportunities (e.g., international tenders).

- The growth/expansion of their product or service sector or the area in which the company has expertise (e.g., computer software, electronics).

- A growing international/external demand for the product/service in question.

- Merging with a company that already had an international focus.

- The low value of the Canadian dollar/exchange rates (making it more attractive for international clients to look for a Canadian supplier with expertise in a particular area).

- Limited opportunities in the Canadian market as a result of domestic market conditions (e.g., the oil industry).

- An opportunity/desire to expand as a result of success in the domestic market.

- Opportunities for more widespread marketing afforded by the advent and growth of digital advertising.

Participants who said their company began immediately with an international focus identified the following kinds of reasons to explain why: the fact that the markets for their products are primarily outside Canada (e.g., mass transit systems, horses and horse products), the ability/opportunity to ‘piggy-back’ on large international/multi-national companies (sometimes as a result of free trade agreements), the need for larger market opportunities to offset production costs/overhead, the opportunity to make more money/profit in larger markets (i.e., outside Canada), and personal experience/contacts.

Increasing profits/sales – main reason for being active in international trade

The most frequently given reason by participants for engaging in international business was (or revolved around) increasing or maintaining sales/profits. Participants routinely offered or identified other reasons, but these accompanying reasons usually linked back to increasing or maintaining sales/profits. For example, participants sometimes identified the following: weak Canadian economic conditions (i.e., not/no longer able to maintain profitability in domestic market alone), being approached by a foreign client (i.e., opportunity to increase profits/enter a new market), and to grow/expand in new markets (i.e., payoff or return on investment is better in larger markets with more clients and more distribution networks).

In some instances, participants noted that what they offer is a niche product or service, designed for specific markets (e.g., products/services designed for earthquake or disaster zones, a breed of horse in demand only in the U.S., products for mass transit systems in large cities). But even in these cases, profitability was a factor. In the case of publishers or novelists, it was also noted that the medium in which they work (i.e., online publishing) is by its very nature international.

Given the centrality of profit a factor motivating companies to seek international business opportunities, it is not surprising that participants’ reasons for being active in international business have not changed substantially over time. What has changed relates to what they have learned or confirmed as a result of their experience in international trade—for example, awareness/understanding of international markets has increased over time, global economic conditions have provided their business/company the opportunity to grow in a way the Canadian market does not offer, and companies have adjusted their marketing approach as a result of entry into the international market (i.e., digital as opposed to print media).

Approaches to international business tend to be part of corporate strategy

Although international business opportunities may have initially arisen in an ad hoc manner, and as a result of circumstances, participants most often described their company’s approach towards its international business activities as part of a plan or business strategy. Representatives of smaller companies and/or companies just recently launched into international trade sometimes described their approach (or part of their approach) as ad hoc (i.e., when and if the opportunity arises) because their situation is still precarious (e.g., they are just starting out, they still go from contact to contract, they have a new distributor and are still ironing out details, they do not want to expand too quickly for fear of exceeding their capacity to meet demand).